9 June 2022

Judy Kwok, Head of Greater China Fixed Income Research

Jane Pan, Director, China Fixed Income Research

Despite market volatility and weakness in Asia’s credit markets, especially the sharp downturn for China properties, the Investment Grade China Local Government Financing Vehicle (IG LGFV)1 sector in the offshore market has delivered relatively resilient performance and recorded a significant increase in net issuance over the year to date. In this investment note, Judy Kwok, Head of Greater China Fixed Income Research and Jane Pan, Director, China Fixed Income Research, highlight the positive drivers behind this bright spot in the China credit space.

With the recent challenging environment in fixed income as global rates have surged, coupled with a prolonged downturn in Asian credits led by the volatile Chinese property sector, investors may be actively searching the region for attractive investment options.

Local Government Financing Vehicles in China (LGFVs), which number around 10,000 in almost every region, may not be as well-known or well-accepted as other asset classes (See the Appendix for background information on LGFVs). In previous years, the opaqueness of some issuers, along with concerns over a mounting maturity wall may have kept some investors away.

We believe, however, that global investors should take a fresh look at LGFVs for several reasons. Those in the investment-grade (IG) space have demonstrated resilient performance thus far in 2022 amid a difficult economic environment. In addition, it is the only corporate issuer to record a year-on-year net issuance increase. Finally, we believe the asset class should benefit from several near-term policy tailwinds moving forward.

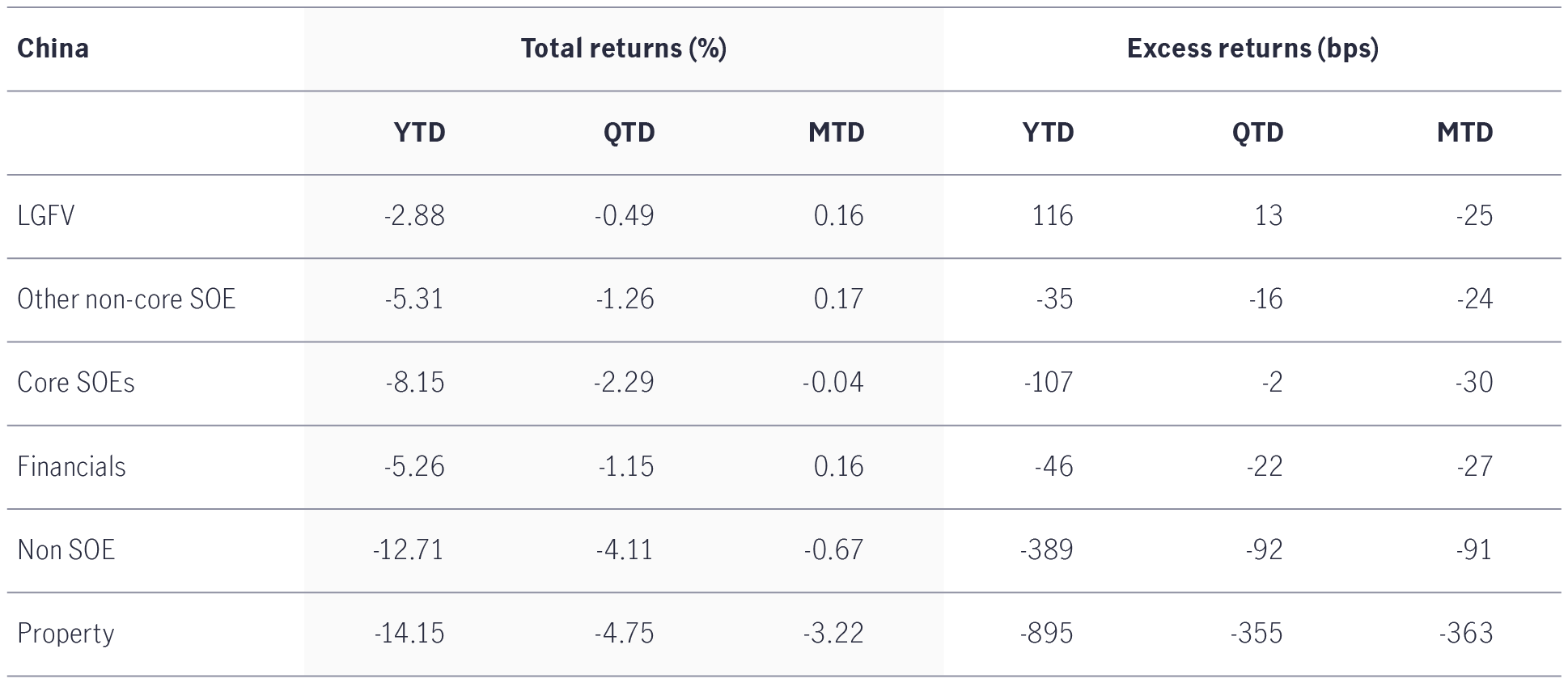

As seen in Chart 1, the China IG LGFV sector registered a total return of -2.9% and an excess return of 1.16% YTD over the US Treasury, making it the best-performing segment in the China IG complex. The sector’s spread has also tightened by more than 40 basis points YTD, which is close to levels last seen in late 2017 and early 20182.

Chart 1: China Investment-grade performance by segment year-to-date3

Looking forward to the second half of 2022 and beyond, we expect the IG LGFV sector’s performance to continue. This could be supported by solid demand from Chinese investors attracted by the yield differentials between the onshore and offshore markets and low supply from state-owned enterprises (SOEs).

Among the IG corporate issuers in China, IG LGFV is a market segment that recorded a year-on-year increase in net issuance: US$12 billion in the first four months of 2022 vs US$3 billion in the same period last year. This sharply contrasts with IG-rated privately owned enterprises (POEs) that saw US$1 billion of net redemption in the first four months of 2022 vs US$12 billion of net issuance in the same period last year4.

At the same time, the Asian US dollar bond market net issuance fell by 91% to US$7 billion in the first four months of 2022, with mainland China recording US$11 billion of net redemptions – in sharp contrast to net issuance of US$30 billion in the first four months of 2021.

Overall, the economic and policy backdrop for the IG LGFV sector also remains supportive. A reduction in LGFV revenue from land sales should be mitigated by stronger support from financial institutions, larger central-government transfers, better earnings from increased infrastructure spending, and the accelerated issuance of local government special bonds. That said, we believe the mandate to control local government “off-balance-sheet debt”5 will remain as some of the debts are too large and strategic to fail.

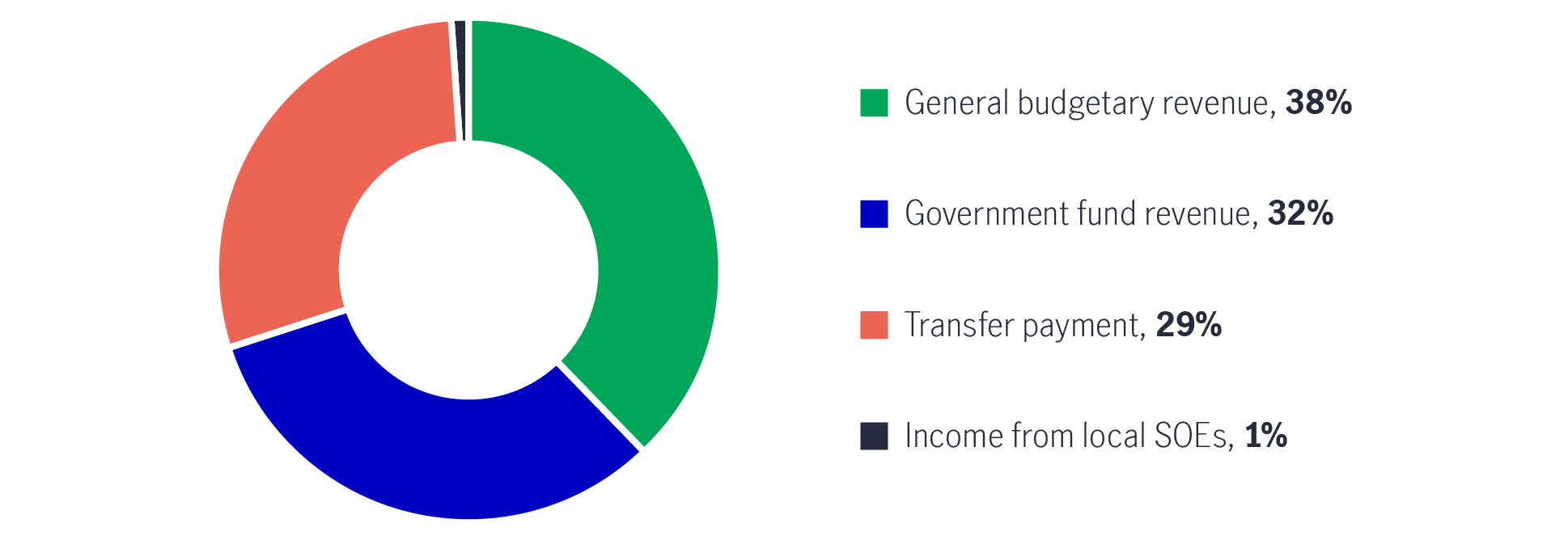

We think consolidated fiscal income of local governments for 2022 is likely to fall. For 2022, the collective forecast6 of 31 provincial governments is a 3% growth in consolidated fiscal income (5% growth for general budgetary revenue, 18% growth for transfer payments from central government7 and a 10% decline for government fund income). This estimate was made before the Shanghai lockdown and, as such, is probably optimistic.

Chart 2: Local government revenue sources, 2022

HSBC, as of end of 2021.

Restrictions on property-developer financing and the enforcement of stricter auction rules had already weakened a key source of income for local governments last year (Chart 2), triggering a decline in land-sale revenue in more than half of China's provinces in 2021.

For 2022, revenue growth from land sales conducted by local governments will likely remain sluggish (our base case is for a 20% year-on-year fall in income from land sales)8. This will reduce an essential source of local-government income, compelling them to rely more on central-government transfers and raise additional debt to finance countercyclical infrastructure spending. Some local governments may need to rely more on LGFVs for financing infrastructure investments while having fewer resources to support them. Besides, lower revenue from land sales will significantly impact regions with less diversified economies and a greater reliance on fixed-asset investment. It will also hit areas experiencing ongoing population outflows given the deduced demand for urban land.9

We believe, the shortfall of fiscal revenue due to weaker land sales and zero-covid policies could be filled by:

As a result of difficult economic conditions, initiatives to deleverage LGFVs are likely to be put on hold for the rest of the year to ensure that 2022 GDP targets are met.

Although China’s growth slowed down to 4.8% in the first quarter of this year (vs the 2022 GDP growth target of “around” 5.5%), infrastructure investment accelerated to 8.5% during the same period (versus 0.4% in 2021). We expect infrastructure-related budget spending and credit to grow by double-digits in 2022 through accelerated issuance of local government specials bonds, pushing infrastructure investment growth to over 10%.

In the past, the risk-reward tradeoff for LGFVs may have seemed less attractive among other alternatives in the China credit universe. Along with a rapidly shifting domestic economic environment, however, a resilient year-to-date performance, coupled with the increasing importance of the sector, and supportive policy tailwinds, might allow some to discover a diamond in the rough.

LGFVs were first established to provide funding for local infrastructure upgrades and prepare parcels of land for sale to property developers. They subsequently expanded into other areas of business related to urban development, such as transportation, utilities, and social housing. LGFVs have ventured into more commercial companies in recent years, including trading, property development, industrials, and finance. As of today. approximately 3,000 local governments issue RMB bonds; 166 issue dollar bonds in the offshore market.

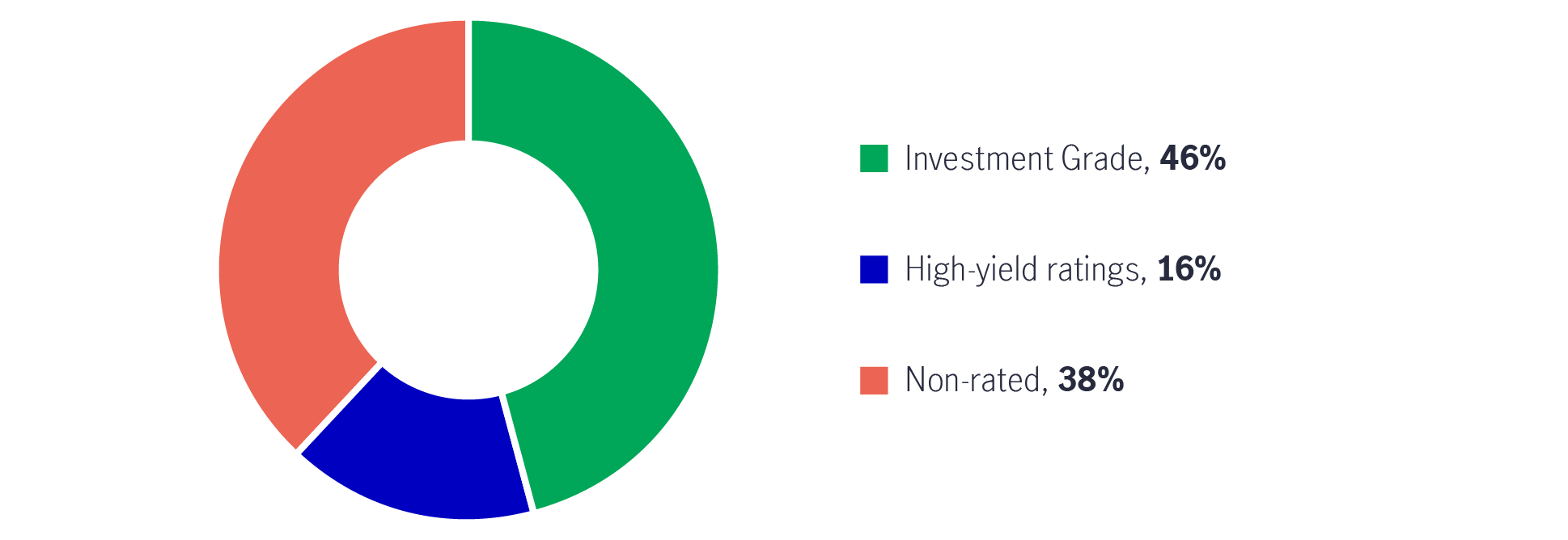

According to their financial reports, LGFV bond issuers had about RMB$45 trillion of interest-bearing debt outstanding as of 2020. This was equivalent to 41% of China’s GDP in 2020, up from 33% in 2016. As of December 2021, LGFVs had RMB$12.6 trillion of bonds outstanding, equivalent to 52% of China’s RMB corporate bonds, up from 35% in 2016. Furthermore, LGFVs now have a sizeable presence in the Asian dollar-bond market, breaking down into IG, high-yield and non-rated segments (see Chart 3) – with US$67 billion outstanding as of 7 March 2022. This was issued by 166 key LGFV dollar-bond issuers (about 6% Asian US dollar bonds and 13% China US dollar bonds)

Chart 3: Ratings of LGFVs10

1. Initially, local governments in China were not permitted to issue debt in their own name, so they created LGFVs to raise funds from the market on their behalf.

2. Barclays Research, 12 May 2022. Spreads are over US Treasuries.

3. Barclays Research, 12 May 2022.

4. On the other hand, high-yield (HY) LGFVs experienced a net redemption of US$421 million in the first four months of 2022 versus a net redemption of US$313 million in the same period last year.

5. Some of the debt raised by LGFVs are kept off the balance sheets of local authorities but carries an implicit government guarantee of repayment.

6. Local governments disclose their fiscal revenue forecasts for each year.

7. According to the Government Work Report, transfer payments from the central government to local authorities will jump by 18% this year to RMB$9.8 trillion. This is one of the largest year-on-year increases in the past decade.

8. Thirty-one provincial governments have budgeted for RMB$7.7 trillion of land-sale income in 2022, down 11% year on year. Among the provinces that generate the most revenue from land sales, Zhejiang estimates a 23% decline from 2021, Jiangsu -19%, while Guangdong was flat.

9. More developed provinces in coastal China and provincial capitals will see a smaller impact because their local governments have a wider range of fiscal revenue to draw upon. The most vulnerable provinces are Inner Mongolia, Shanxi, Gansu, Heilongjiang, Jilin, and Liaoning.

10. HSBC Research, March 2022.

Asset allocation views on SpaceX IPO, Reopening of Strait of Hormuz, and the BOJ rate hike

The Multi Asset Solutions Team (MAST) provides asset allocation views on three recent developments that could influence markets in different ways: the SpaceX Initial Public Offerings (IPO), the reopening of the Strait of Hormuz, and the Bank of Japan’s (BOJ) rate hike. In our view, these events create mixed signals across growth, inflation and liquidity. Overall, the backdrop still appears uneven, and this may support a measured and selective approach to asset allocation rather than a broad increase in risk.

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

Asset allocation views on SpaceX IPO, Reopening of Strait of Hormuz, and the BOJ rate hike

The Multi Asset Solutions Team (MAST) provides asset allocation views on three recent developments that could influence markets in different ways: the SpaceX Initial Public Offerings (IPO), the reopening of the Strait of Hormuz, and the Bank of Japan’s (BOJ) rate hike. In our view, these events create mixed signals across growth, inflation and liquidity. Overall, the backdrop still appears uneven, and this may support a measured and selective approach to asset allocation rather than a broad increase in risk.

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()