11 October 2021

Edward Ritchie, Senior Portfolio Manager of Japan Equities

At first glance, corporate governance in Japan seems to have hit a nadir in the past couple of years, with at least two prominent firms—Nissan¹ and Toshiba²—making headlines globally for the wrong reasons. However, according to Edward Ritchie, Senior Portfolio Manager of Japan Equities, a closer examination shows that things are indeed changing in Japan, albeit at a slow pace.

Shareholders and corporate boards now have greater control over dominant and seemingly immovable company chairs and chief executive officers (CEOs) than before. In our opinion, the recent spate of governance scandals hitting Japanese corporates should be seen as a symptom of the steady improvement in corporate governance practices in the country. These improvements have created a way for companies to hang their dirty laundry in public—something that would be deemed inconceivable as recently as five years ago—which will be good for everyone in the long run.

As corporate Japan becomes more globalized and less homogeneous, the need for greater governance exists not only for good practice, but also to maintain trust between employees and shareholders. Historically, Japanese employees would only work for one company in their professional life and, as such, they were intensely loyal to their employer and senior managers in the firm. Likewise, shareholders would typically have long-standing relationships with the company, and their shareholding could represent just one part of their relationship with the firm—they may also be creditors, suppliers, or customers. This model is slowly changing.

More and more Japanese workers are changing companies during the course of their career as they increasingly prioritize factors such as mobility and a sense of fulfillment over stability.³ This has reduced the traditional sense of loyalty that Japanese workers feel toward their employers. It’s a development that has created an opportunity for new employees to introduce new concepts of best practices that they may have encountered in their previous jobs and helped to foster a culture in which staff members now feel able to speak out when they’ve noticed fraudulent activities. The changing culture of working in Japan is having a positive impact on Japanese corporate governance, and policies to support whistleblowers in Japan are catching up too. The Whistleblower Protection Act was passed in 2006, but general awareness of whistleblower rights and protections has been insufficient. This led to amendments to the Act last year, which have helped to broaden the scope of these protections.⁴

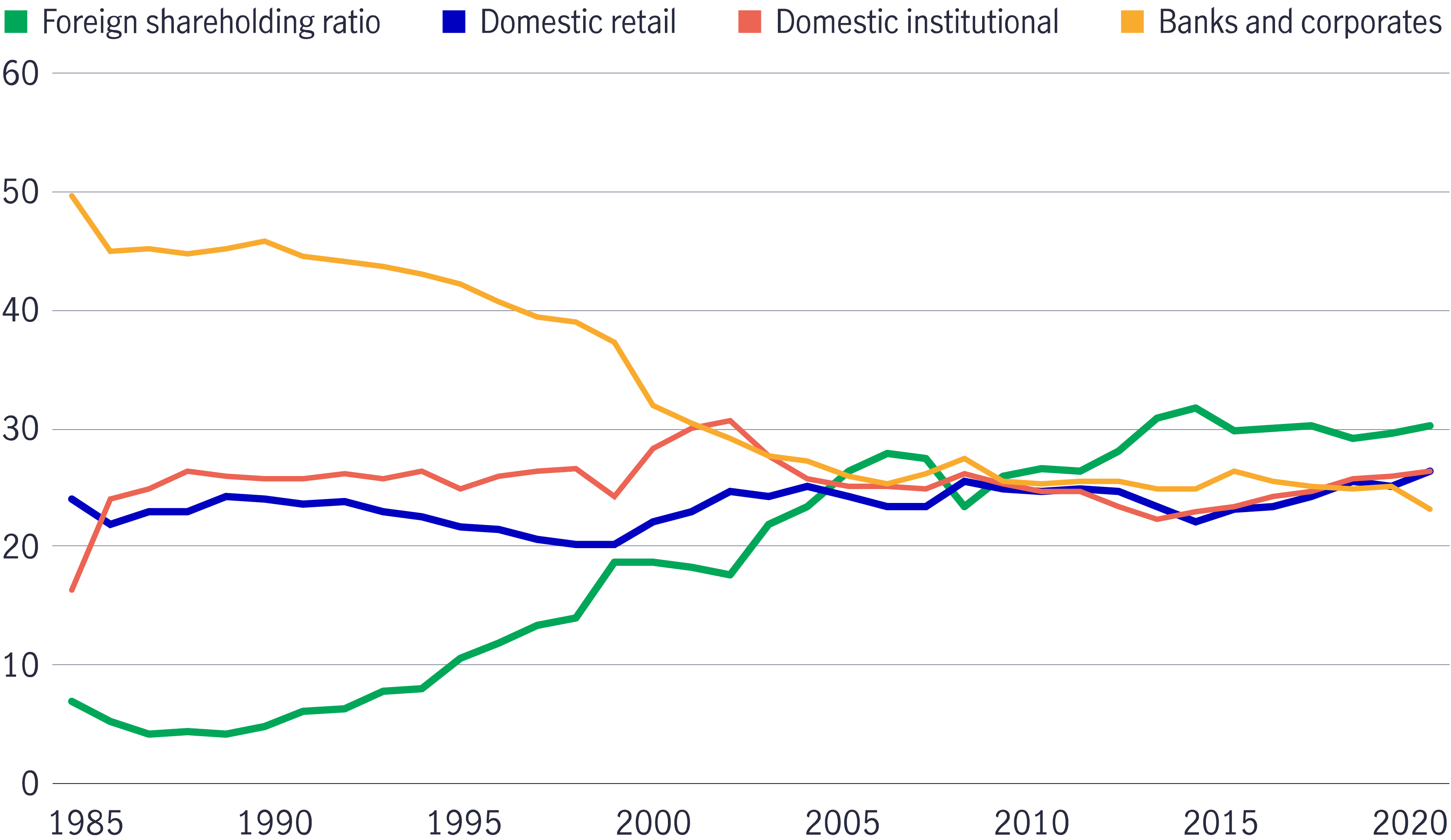

Composition of shareholders in Japanese firms is changing

Source: CLSA, Manulife Investment Management, as of July 2021.

The composition of shareholders is also changing as foreigners increase their share of ownership in Japanese companies, while banks and corporates in the country come under greater pressure to reduce their shareholdings, which is widely seen as an inefficient use of capital. This has also meant that, increasingly, shareholders have only a single relationship with the firm they’re invested in—as a partial owner and nothing more.

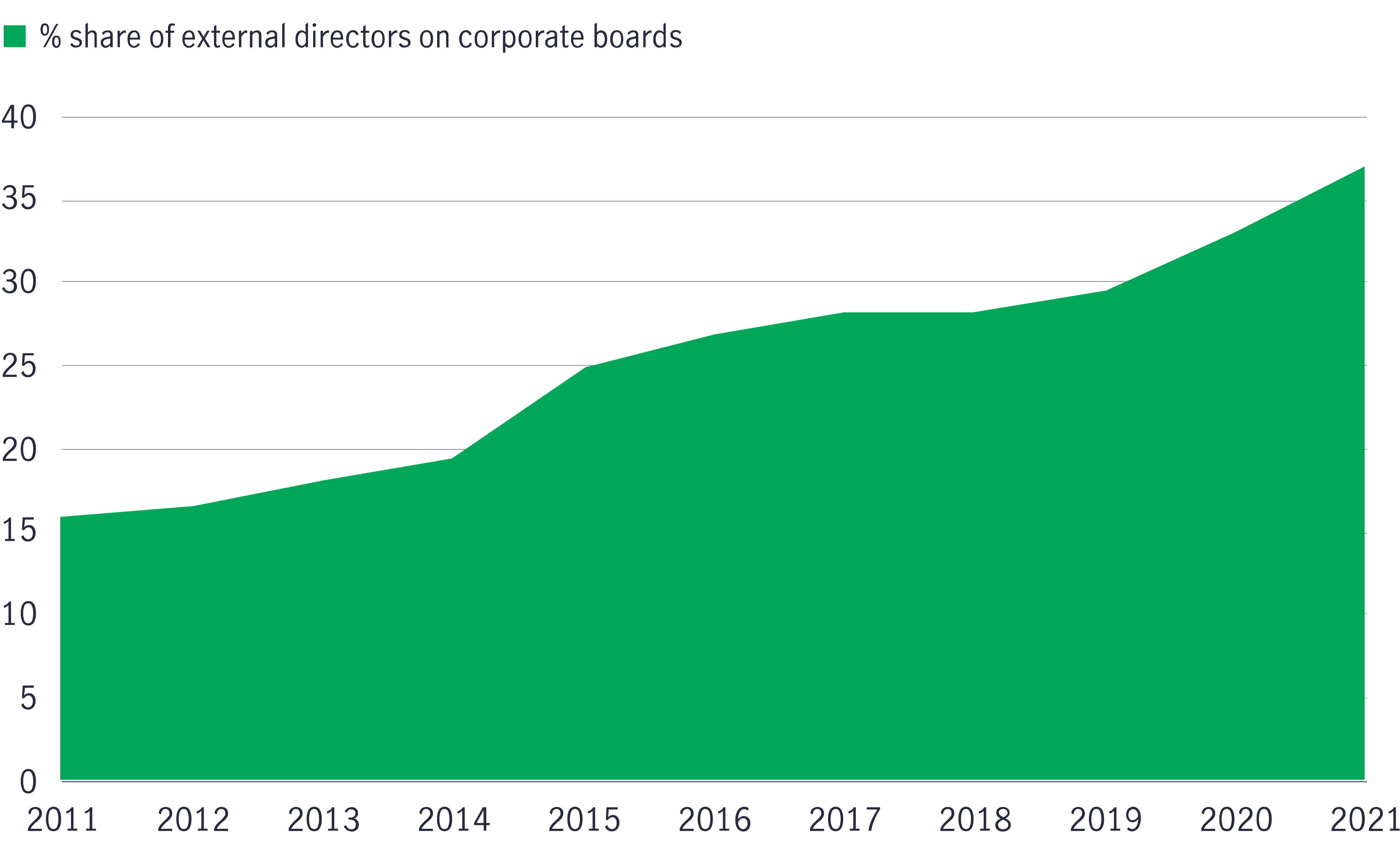

Japan has significantly increased the number of external directors over the last few years. For instance, in 2014, only 21.5% of companies listed on the Tokyo Stock Exchange and the Osaka Stock Exchange had at least two external directors, but by 2020, the figure rose to 95.3%.⁵ We believe this has been driven by the introduction of Japan’s corporate governance code in 2015, which insists on no less than two genuine external directors on corporate boards. However, many of these external directors have been lawyers, university professors, and accountants who appear to have limited influence over the power vested in the president/CEO of a firm.

Board composition in Japan Inc.: an improving picture

Source: Board Director Training Institute of Japan, Manulife Investment Management, July 2021.

According to the Asian Corporate Governance Association, Japan’s corporate governance ranking within Asia rose to fifth place in 2020, up two places from the previous exercise in 2018.⁶ On the surface, the improved showing indicates progress; however, a closer examination shows that the country’s higher ranking in 2020 had more to do with its efforts related to climate change disclosure. Crucially, the country continues to rank below Australia, Hong Kong, Taiwan, and Singapore. We believe the recent uproar over Toshiba also underscores the fact that even genuinely independent directors can find it difficult to break board consensus built around the CEO.

In 2006, Hiroshi Okuda, former chairman of Toyota, was quoted as saying that there’s no need for outside directors, as they don’t understand the company or the industry and “would just get in the way.”⁷ We respectfully disagree, Mr. Okuda: Outside directors are there to protect the interests of shareholders and stop powerful management from abusing its position. In a sign of how things have changed in the 15 years since Mr. Okuda left the firm, Toyota has devoted much of its effort into overhauling its corporate governance structure and has named three external members to its board of directors.⁸

Female representation in Japan's board room is rising

Source: Board Director Training Institute of Japan, Manulife Investment Management, July 2021.

In the past few years, we’ve also seen encouraging signs that things are moving in the right direction. Sony, for example, has fully embraced the concept of outside directors, with a majority of the board being such. This change was made in 2014,⁹ at a time when the company was incurring losses in many of its divisions. Although the outside directors weren’t able to advise on the business itself, they did advise on the need to remove the silo mentality among the company’s different divisions. Over the course of the last four years, the company has seen its underlying earnings rise significantly.

Nearly 44% of TOPIX 500 Index companies have separated the role of the company chair from the CEO in 2020, up from roughly 41% in 2010.¹⁰ This shows that the progress in this area has been slow. One other area of concern—of those that had already separated the chair/CEO roles, roughly 74% of them have invited a former CEO (or equivalent) to remain on the board of directors. This may suggest that transfer of power, or true purpose of separating both roles, may not yet be complete. The way we see it, while these companies have certainly made some progress in regard to improving corporate governance, they still have some ways to go.

Chair/CEO role separation: progress made, but could be better

| TOPIX 500 Index companies | 2010 | 2020 |

| Share of firms that have introduced chair/CEO role separation | 41% | 44 |

| Share of firms whose board comprises at least 30% independent directors | 9% | 77% |

| Share of firms whose board comprises at least 50% independent directors | 2% | 14% |

| Share of firms whose board comprises at least 75% independent directors | 0% | 1% |

| Share of firms that have split chair/CEO roles but retained former CEO on board of directors | 82% | 75% |

Source: Bloomberg Finance L.P., June 2021.

Although a separation of roles is encouraged, it’s also possible to strengthen governance while retaining a combined chair/CEO role through a firm’s committee structure: If a company has a single chair/CEO, its committees should be chaired by other board directors, preferably external directors. A good example of this structure is Hoya Corporation, where the company CEO also assumes the role of the chair, but its audit, nominations, and remuneration committees are each chaired by one of the company’s independent directors.¹¹

Japan’s historical system of setting up a parent company with various subsidiaries has brought about many instances of management abuses of control. In many instances, subsidiaries are no more than sales agencies for the parent company and aren’t directly attached to the parent company’s corporate governance rules. Where controls are loose, there have been instances in which sales subsidiaries have overstated sales figures in order to meet targets set by the parent company—this is one of the primary causes of accounting scandals in Japan.

This was the primary cause of the recent accounting scandals at Hoshizaki Corp,¹² a manufacturer of ice machines and commercial refrigerators that struggled to reconcile its earnings as both a domestic and overseas subsidiary had overstated sales.

In the case of listed subsidiaries, the abuse of control can come from the parent company itself—it can demand its subsidiary to make capital expenditures for its own benefit, or even take direct control over the subsidiary’s cash flow.

In our view, the best solution is to reduce Japan Inc.’s reliance on the subsidiary structure, and this is starting to happen: Hitachi, one of Japan’s largest electronics conglomerates, sold its 51% stake in its listed chemical business in 2019;¹³ more recently, the company’s been contemplating buying out the remaining minority stake of its semiconductor capital equipment business. Other Japanese conglomerates are following suit, partly due to Hitachi’s success and changes in TOPIX listing rules, which will lead to a reduction in the index weighting of subsidiaries with large corporate ownership.¹⁴

However, the process of buying back minority stakes can be complicated, as minority investors may feel that the parent company is taking advantage of its position to buy out minorities at a heavily discounted valuation. This happened when Panasonic offered to make PanaHome a wholly owned subsidiary in 2017.¹⁵ PanaHome’s second-largest shareholder demanded a better deal, noting that the offer that was on the table undervalued the firm by more than 50% and called the transaction a test case of whether Japan’s corporate governance overhaul is working. Panasonic eventually raised its bid by 20% and increased the cash component of its offer.¹⁶ This, along with other more recent cases, is a good example of how the subsidiary structure can lead to a serious undervaluation of assets, unfairly penalizing those who own a minority stake in the listed subsidiary.

Investor activism is a controversial subject that isn’t always looked on kindly within the business community, and perhaps even more so in Japan, where the country’s most famous activist investor, Yoshiaki Murakami, was found guilty of engaging in insider trading.¹⁷ Mr. Murakami’s conviction and allegations of greenmailing—the practice of amassing shares in a firm with the objective of forcing the firm to buy back its own shares at a premium to fend off a hostile takeover—have given the cause a bad name in the country.

As a result, many Japanese companies have resorted to introducing so-called poison pill clauses, which allow existing shareholders to buy additional shares at a discount, thereby raising the cost of any potential takeover, to fend off unwanted offers. This has, in many ways, set the country back significantly in terms of improving corporate governance since these clauses can also be used as a management tool to resist changes that might be needed.

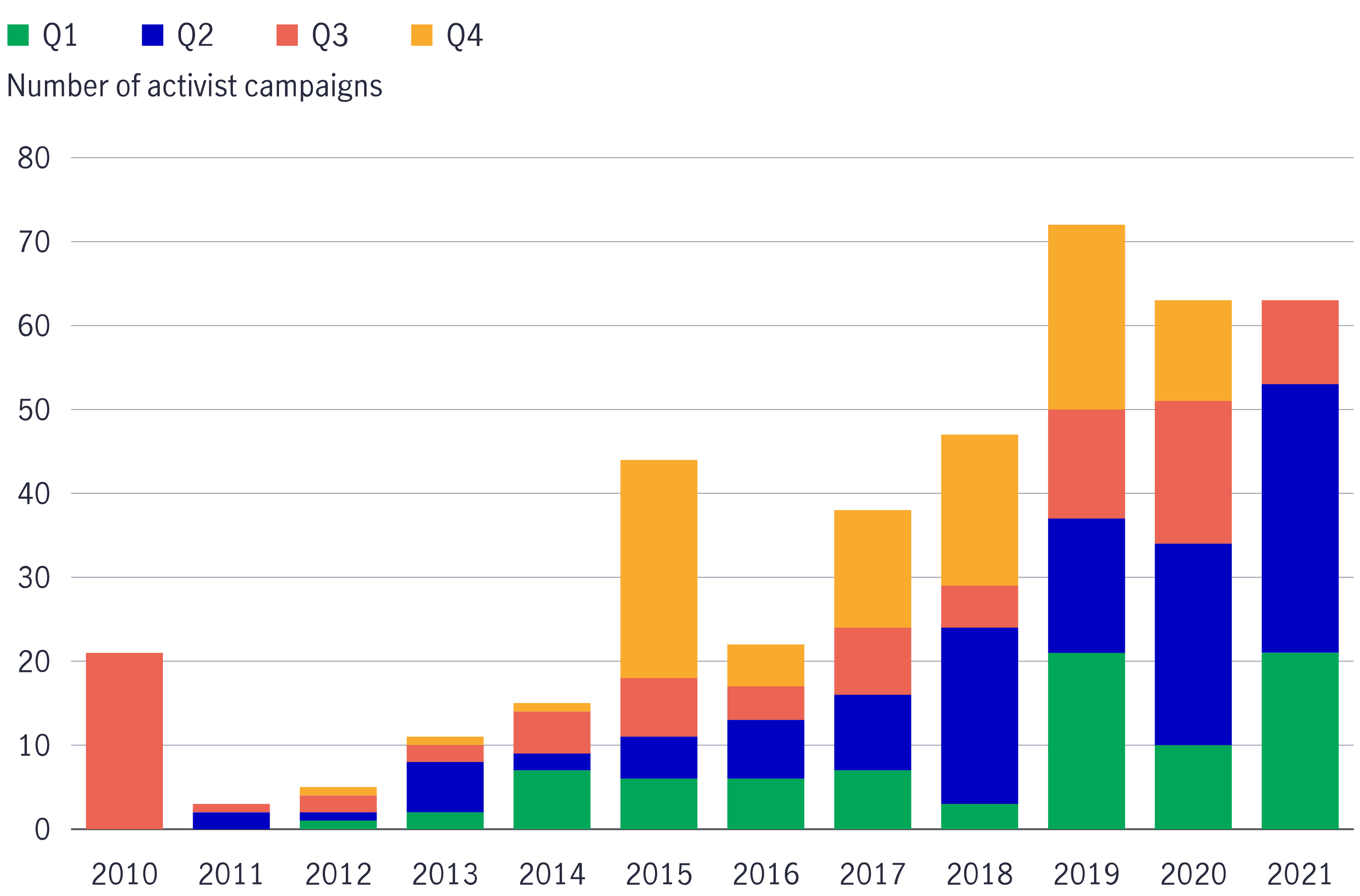

That said, investor activism in Japan has a different face today: It’s more focused on improving governance and removing poor-performing management than on making a quick buck. In fact, Japan has consistently ranked second (with 2018 being an exception) in terms of shareholder activism since 2015.¹⁸

Investor activism is gaining momentum in Japan

Source: Bloomberg, CLSA, as of August 24, 2021.

In the last 12 months, activists have targeted specific companies that were failing to meet return-on-equity (ROE) targets or where top management had unwarranted control of the board. Recent examples include optics manufacturer Olympus, which was pressured into appointing three foreign board directors following a two-year-long campaign by a U.S.-based activist investor.¹⁹ The reappointment of Kinya Seto as CEO of Lixil Group also represented a high-profile victory for corporate governance in Japan. Mr. Seto was hired to turn the firm around but was “misled into resigning”²⁰ after clashing with one of the firm’s founding families; however, he resecured his job through a shareholder proposal. In our view, the message couldn’t be clearer: Japan has made important progress on the governance front, and investor activism has shed some of its negative associations.

Indeed, investor activism is now more common in Japan—changes in shareholder structure (the rise in the proportion of nonaligned shareholders within a firm) have given activists a stronger platform to encourage change at the board level through proxy voting. Clear investor policies on proxy voting and key environmental and social issues are now encouraged by government agencies such as Japan’s Government Pension Investment Fund (the country’s largest public investor), adding heft and credibility to the movement.

Asset allocation views on SpaceX IPO, Reopening of Strait of Hormuz, and the BOJ rate hike

The Multi Asset Solutions Team (MAST) provides asset allocation views on three recent developments that could influence markets in different ways: the SpaceX Initial Public Offerings (IPO), the reopening of the Strait of Hormuz, and the Bank of Japan’s (BOJ) rate hike. In our view, these events create mixed signals across growth, inflation and liquidity. Overall, the backdrop still appears uneven, and this may support a measured and selective approach to asset allocation rather than a broad increase in risk.

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

Japan’s Financial Services Agency set up a Council of Experts in 2014 to set out a Stewardship Code for institutional investors. The code prescribes that institutional investors should participate in “constructive engagement with investee companies.”²¹ Although the wording is somewhat vague, it’s opened a path for constructive communication between Japanese management and investors. Once again, we’re seeing progress on this front: As of June 2021, 309 institutional investors have signed up to the code, a marked improvement from the 221 signatories just three years prior.²²

Japan’s Stewardship Code: growing support

| Signatories | February 2018 | June 2021 |

| Trust banks | 6 | 6 |

| Investment managers | 158 | 199 |

| Insurance companies | 22 | 24 |

| Pension funds | 28 | 68 |

| Others | 7 | 12 |

| Total | 221 | 309 |

Source: Financial Services Agency (Japan), June 2021.

Core to our investment philosophy is the belief that a vibrant and challenging management team will lead to a healthy business and that a company’s board structure provides a template for achieving this objective. As such, we’re committed to engaging with management teams of our investee firms to ensure that certain criteria for board composition are met. These include:

We’ll use our proxy voting rights to ensure that these criteria are being met, or that a clear policy is in place setting out how and when the criteria will be met.

There are signs that corporate governance is improving in Japan, despite the negative news flow. Board structures have improved and external directors are having a greater influence on board decisions. We believe the recent announcement by Dai-Ichi Life to buy back up to 15.25% of its outstanding shares²³ was the result of a combination of activism, the support of its external directors, and top management that’s willing to pay attention to shareholders’ interests.

Corporate culture is also changing with less emphasis on lifetime employment, which is replaced by a growing focus on skilled workers who can innovate and generate new business opportunities. Our analysis shows that apart from last year, when the COVID-19 outbreak constrained economic activities, ROE for Japanese stocks has been rising consistently since 2016. In our view, this is partly due to improvements in corporate governance and culture. Crucially, we believe these changes have taken root, and we should see further improvements in the years to come.

1 “The Rise and Fall of Carlos Ghosn: Part 1,” Harvard Business Review, June 3, 2021.

2 “Toshiba’s chairman resists calls to resign, to bring in new directors,” Reuters, June 14, 2021.

3 “Changes in job change rate,” Transtructure, February 9, 2021.

4 “Are Whistleblowing Laws Working? A Global Study of Whistleblower Protection Litigation,” International Bar Association, March 2021.

5 “Abenomics improved Japan’s corporate governance, but more work remains,” Japan Times, September 14, 2020.

6 “CG Watch 2020: Future Promise,” The Asian Corporate Governance Association, May 20, 2021.

7 Japan Remodeled: How Government and Industry Are Reforming Japanese Capitalism, page 167, Steven Vogel, Cornell University Press, 2006.

8 “Corporate governance at Toyota Motor Corporation,” Toyota Motor Corporation, June 24, 2021.

9 “Notice of the Ordinary General Meeting of Shareholders to be held on June 19, 2014,” Sony Corporation, June 2, 2014.

10 Japan Exchange Group, as of July 2021.

11 “Leadership: Board of Directors,” www.hoya.co.jp/english/company/directors.html, June 29, 2021.

12 Bloomberg, October 2018.

13 “Hitachi to sell chemical unit and diagnosis imaging equipment units,” Japan Times, December 19, 2019.

14 “Tokyo’s Promise of Generational Stock Revamp Draws Skeptics,” Bloomberg, February 8, 2021.

15 “Hedge Fund Oasis Pushes for a Better Panasonic-PanaHome Deal,” February 20, 2017.

16 “Panasonic raises PanaHome buyout offer to appease shareholders,” Reuters, April 21, 2017.

17 "Japan financier Murakami jailed for insider trading,” Reuters, July 19, 2017.

18 Bloomberg, Morgan Stanley Research, as of August 4, 2021.

19 “US fund ValueAct forces Olympus to appoint 3 foreign directors,” Financial Times, January 11, 2019.

20 “Former CEO of Japan’s Lixil returns after governance tussle,” Reuters, June 25, 2019.

21 “Principles for Responsible Institutional Investors: Japan’s Stewardship Code,” Financial Services Agency (Japan), March 2020.

22 Financial Services Agency (Japan), June 30, 2021.

23 “Notice Regarding the Repurchase of the Company’s Shares,” Dai-ichi Life Holdings, March 21, 2021.

![]()