24 February 2023

Steven Slaughter, Lead Portfolio Manager

Following impressive performance in 2021, global equities experienced pressure in 2022 as the economy pushed forward with its recovery from the COVID-19 pandemic. Decades-high inflation and aggressive central bank monetary tightening dragged equities and corporate profit estimates lower amid growing fears of a recession. The conflict between Russia and Ukraine and persistent COVID outbreaks also weighed on investor sentiment. In this 2023 outlook, Steven Slaughter, Lead Portfolio Manager, discusses the attractiveness of allocating to the healthcare sector in the current economic environment and outlines why it warrants a long-term allocation.

As we entered 2022, global markets reflected a sense of optimism for stability and continued economic recovery following the historic volatility witnessed throughout 2020 and 2021 as a result of the COVID pandemic.

However, 2022 proved far more turbulent than expected. Multiple adverse events impacted global markets and the economy as they continued to grapple with a persistent COVID environment. These incremental headwinds included Russia’s invasion of Ukraine and supply-chain issues that exacerbated surging inflationary pressures. Central banks were forced to pivot to aggressive monetary tightening, which weighed on investor sentiment and triggered mounting fears of a global economic recession.

There were few places to hide in this challenging environment, as broader equity and fixed-income markets experienced steep losses. Yet, the healthcare sector offered relative protection during the drawdown, once again proving itself a defensive stalwart for investors.

Notwithstanding the sector’s relative outperformance in 2022, we believe that healthcare remains an attractive investment in 2023 and over the long-term. Its resilient qualities should help it outperform the broader equity market through a full market cycle, while its propensity for ground-breaking innovation will provide strong growth avenues.

While COVID-19 related advancements have been the focus of the healthcare landscape recently, the pursuit of treatments and advancements for other unmet medical needs remains a core focus of the industry – these include cancer, metabolic syndromes, rare or orphan diseases, and central nervous system (CNS) disorders, to name a few.

Furthermore, emerging evidence of the health outcomes of patients previously infected with COVID increases the importance of addressing such unmet medical needs.

Indeed, the ability of healthcare companies to address such unmet medical needs is one of the three guiding principles by which we allocate capital and helps inform the sector’s impressive long-term growth prospects moving forward.

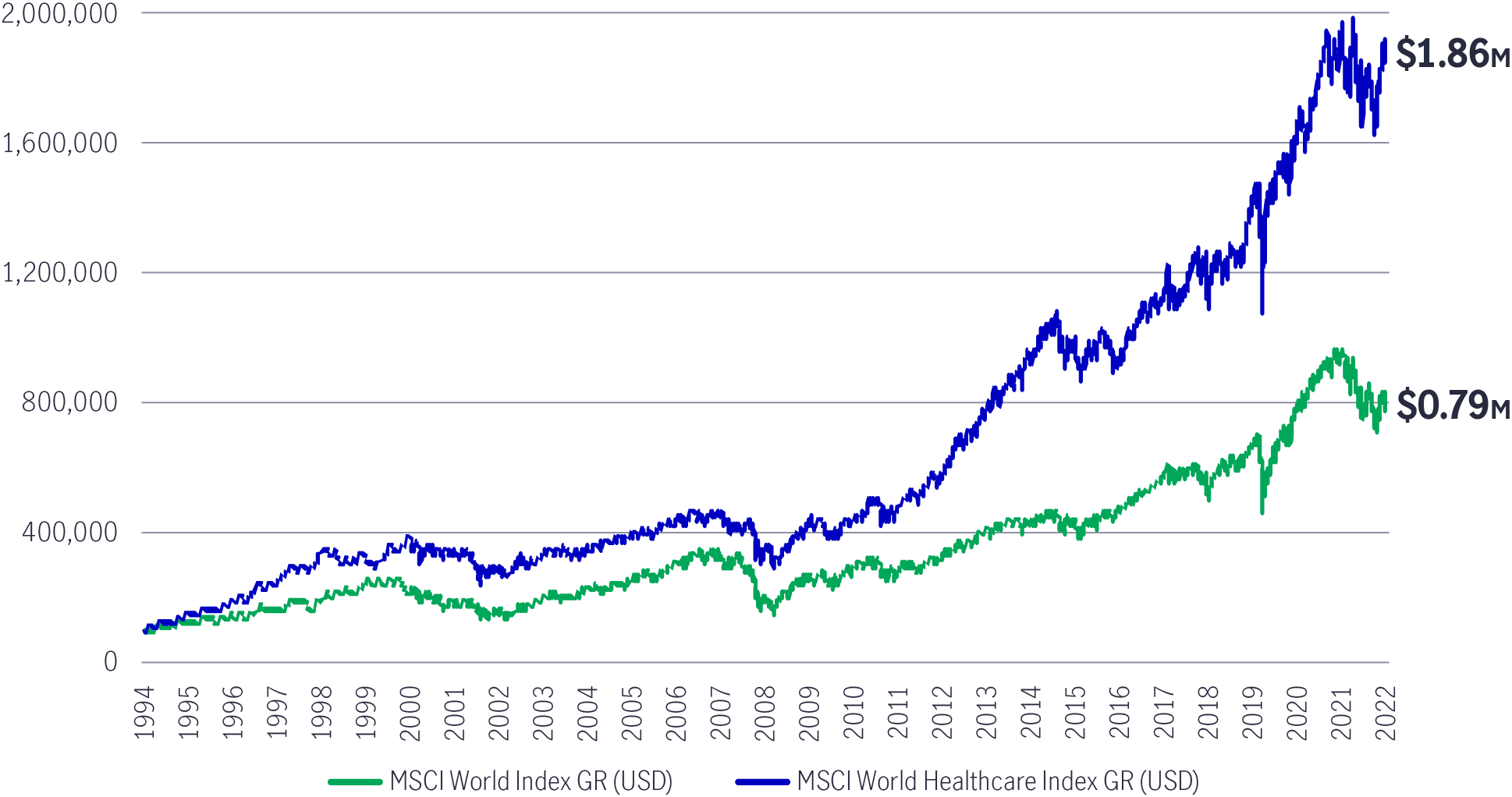

Chart 1: Investment growth for every US$100,000 from 31 December 1994 to 31 December 2022

Global healthcare equities have outperformed the broader market by over 3% (annualised) since 1995 – a difference that really adds up

Source: eVestment, as of 31 December 2022.

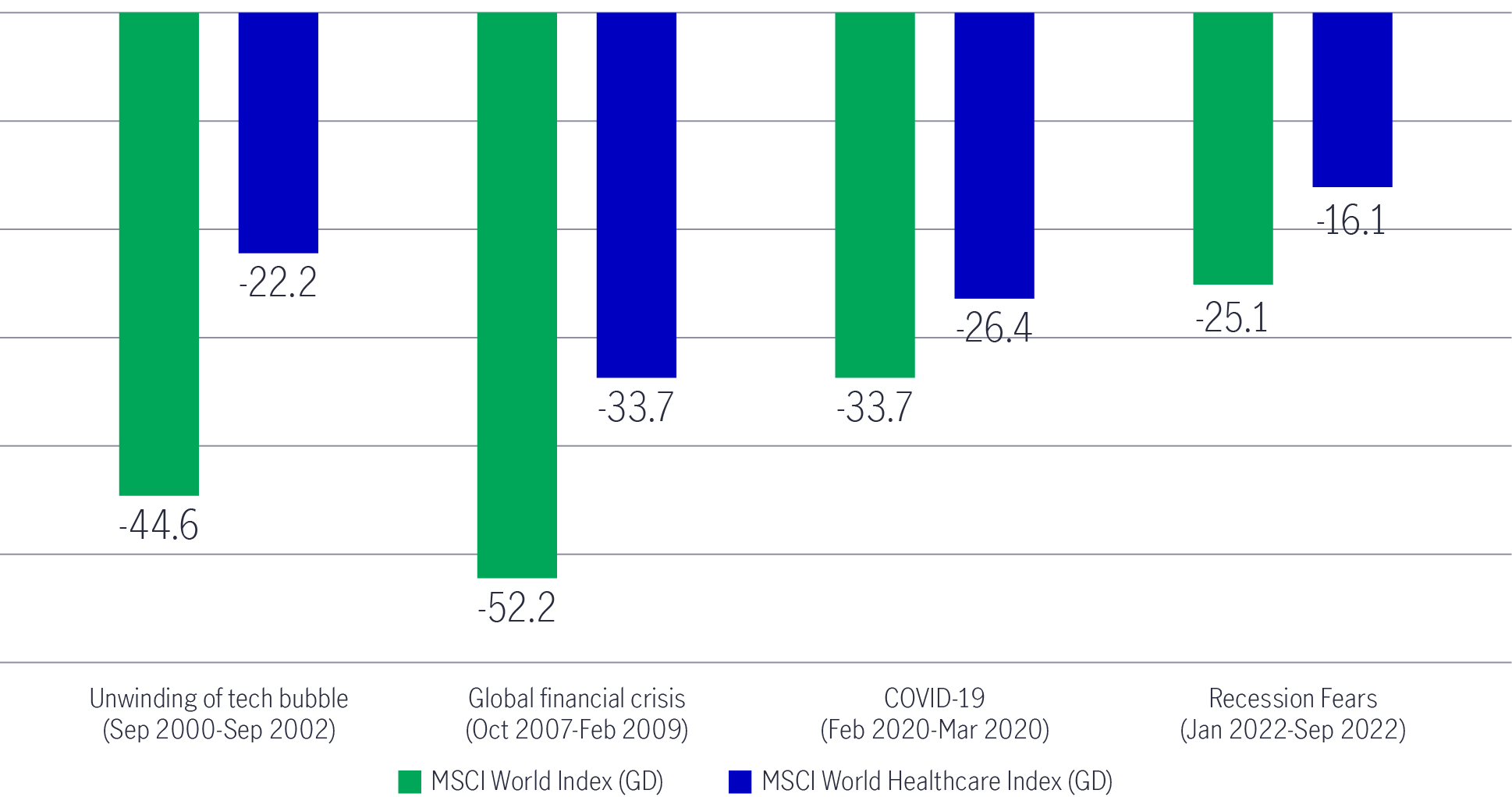

Healthcare has historically delivered strong outperformance throughout economic cycles, particularly during downturns. These excess returns tend to be more pronounced during periods of heightened market volatility and economic distress. The challenging environment experienced in 2022 was no different, with the sector delivering strong relative excess returns.

Chart 2: Healthcare’s excess returns are more pronounced during economic downturns

Source: eVestment, as of December 2022.

The sector’s defensiveness stems from the supply-and-demand dynamic of healthcare products and services. While cyclical industries usually experience a sizable reduction in demand during economic downturns, healthcare demand generally remains resilient, with consumers having an inelastic appetite for biopharmaceutical products, medical goods and services. This was even more pronounced during the COVID-19 pandemic, with many healthcare products and services experiencing a surge in demand.

While it’s uncertain whether we will see a major global economic recession in 2023, we believe the healthcare sector to offer investors a relatively safe place for their capital if a recession ultimately occurs.

Our fundamental research process has uncovered several noteworthy clinical trials demonstrating increased morbidity in patients recovering from previous COVID infections (so-called “long COVID”). These studies have specifically identified the elevated risks of cardiovascular diseases, diabetes, and CNS diseases among patients subjected to previous COVID infections (relative to the uninfected population).

While the long-term implications of these findings will require further research, we believe the consistency of these findings (from multiple researchers) suggests increased underlying demand for relevant biopharmaceutical and medical products in a post-pandemic world.

In recent years, COVID-19-related advancements have been the focus of the healthcare landscape. In record time, the world’s leading healthcare companies developed effective vaccines, diagnostic tests, and therapeutics to combat the virus. Additionally, new technological advancements in telehealth allowed doctors to connect remotely with patients as the pandemic spurred innovation across the industry.

While most of the world is seeing lower hospitalisations, deaths, and better treatment of the virus, China and certain other territories have seen a surge in cases, and we would expect these fluctuating spikes to continue in various geographies as the transition to a seasonally endemic virus unfolds.

The remarkable response of the healthcare industry to the pandemic has generated incremental returns due to sales of the vaccines, diagnostics and therapeutics mentioned above. As anticipated, many of these companies have, in turn, reinvested excess cash flows to augment their discovery capabilities, capital spending, and pipeline investments, thus compounding further advances in non-COVID unmet medical needs.

As we transition to a post-COVID environment, we expect innovation to accelerate across the sector and believe it is poised to reap the rewards of these incremental investments.

Rigorous fundamental research that sifts through vast swathes of scientific data is paramount when allocating capital in this sector. A bottom-up, fundamental investment process informed by the assessment of emerging scientific and medical developments, coupled with a disciplined intrinsic valuation framework, has the potential to uncover robust opportunities for investors at fair valuations.

This approach continues to inform how we evaluate investment opportunities across the healthcare universe. To this end, the findings mentioned above relating to structural changes in healthcare (including, but not limited to, long COVID) support the urgency to effectively manage other pre-existing disease states (cancer, metabolic syndromes, asthma, and other immunologic disorders) that our research suggests pre-dispose these comorbid patients to higher morbidity and mortality from COVID-19.

Accordingly, this has led us to increase our conviction in biopharmaceutical companies that are over-indexed to cardiovascular disease, Alzheimer’s, and diabetes at the present time.

Secondly, we maintain a positive view on several diagnostics and tools companies, as well as biopharmaceutical firms, that we believe will continue to reap the benefits of excess cashflows consistent with the emerging endemic state of COVID. Several of these names will generate above-market returns as the incremental research, capital spending and pipeline investments they have implemented reach fruition.

For example, a diversified healthcare products company has invested substantial incremental profits from its COVID testing business to advance a market-leading position in continuous glucose monitoring – an emerging diagnostics modality and underappreciated market opportunity in Type-2 diabetes.

Finally, and as previously noted, we have a negative view towards select biopharmaceutical, healthcare services, and medical device companies that are over indexed to various disease states and product markets disproportionately and adversely impacted by the persistent COVID environment. These include companies with exposure to elective surgeries, hospital services, and select oncology conditions.

We believe that new modalities in treatment and prevention will continue to drive long-term governmental outlays toward healthcare products and services. Irrespective of the incremental tailwinds and headwinds associated with COVID-19, the underlying secular trends of ageing demographics, medical advancements, and profound unmet medical needs continue to support long-term exposure to global healthcare companies in a well-balanced investment strategy.

Select companies within the healthcare space offer the potential for strong, long-term outperformance. As such, this is an opportune time to invest in the sector, with a focus on the importance of stock selection as a potential driver of outperformance. We believe these innovative and compelling companies can survive the next market downturn and create long-term value for shareholders.

A bottom-up fundamental investment process informed by assessing emerging scientific and medical trends, coupled with a disciplined intrinsic valuation analysis, can uncover these robust opportunities. This approach should ensure that capital allocation focuses on companies tackling important unmet medical needs, pursuing underappreciated market opportunities or demonstrating an ability to bend the healthcare cost curve.

Global Macro Outlook Q3 2023: The long and winding road

At the time of writing, only the eurozone and New Zealand have slipped into recession (as defined by two consecutive quarters of negative growth). But don’t pop the champagne just yet: We see this as a case of recession postponed rather than canceled. Read more.

Asian High Yield: Building resiliency amid volatility

Although emerging from a difficult period, Asian-high-yield is positioned to weather the current market volatility due to regional economic strength and unique asset class characteristics.

What’s next for China’s property sector?

The road ahead is likely to be bumpy but select opportunities still exist in the US-dollar high-yield bond space. Robust credit selection and valuation assessment have become even more important considerations in the current market environment.

2026 Mid-year outlook: Global Semiconductor

The semiconductor sector remains a key enabler of the global economy, underpinning artificial intelligence (AI), cloud computing, and electrification. As highlighted in our earlier insights, it represents a broad ecosystem supported by structural demand and real infrastructure investment. Following strong year-to-date performance, we see growing conviction that momentum can extend into the second half of 2026 and into 2027, driven by earnings strength, sustained capital investment, and early-stage AI adoption.

2026 Mid-Year Outlook Series: GEDI

Against a highly uncertain backdrop in the first half of 2026, Manulife’s Global Equity Diversified Income (GEDI) Fund (‘the Fund’) posted resilient performance with relatively lower volatility. This result was driven by the Fund’s four investment pillars, which favour an income-centric approach, coupled with global diversification across growth, value, and income equities. In this 2026 Mid-Year Outlook, Paul Kalogirou, Head of Client Portfolio Management, Asia & Global Multi-Asset Solutions, explains how the Fund’s unique structure allows for consistent income generation and potential upside across the market cycle, while also identifying key opportunities and risks for the second half of the year.

2026 Mid-year Outlook Series: Diversified Real Assets

Global supply chains are resetting under deglobalisation and geopolitics, shifting from global efficiency to more expensive regional resilience, embedding higher structural costs. At the same time, artificial intelligence (AI) is emerging as a new demand driver, accelerating investment in power, infrastructure, and materials. Against this backdrop of structurally higher inflation and dual demand pressures – from both supply-chain rewiring and AI capital expenditure – we believe real assets may play an increasingly important role in portfolios, offering exposure to long-term secular growth and AI trends.

![]()