The global spread of coronavirus (COVID-19) has sent shockwaves through global equity markets. The impact, however, has been unevenly distributed, providing opportunities for investors. In this investment note, Rana Gupta, Indian Equities Specialist, offers his outlook on Indian equities. Overall, he believes that despite near-term volatility, the country’s robust foundation of structural reform, domestic nature of the market, and prudent monetary and fiscal policy, should help it to navigate the currently challenging market environment.

India currently faces notable short-term challenges, including the outbreak of COVID-19 and the preceding slowdown of the informal economy. In this note, we review the current situation, the response from policymakers, and how both issues impact our views. Finally, we focus on why investors should remain focused on positive long-term themes in India.

The COVID-19 pandemic is an unprecedented global health crisis, and its impact is likely to dominate global markets and policymakers' attention in the near term.

Until February, India was relatively less impacted by COVID-19 than other countries. After the World Health Organization (WHO) declared it to be a pandemic, the Indian government imposed several restrictions1 and subsequently announced a nationwide lockdown on 24 March that is scheduled to end on 3 May.

The total number of confirmed cases in India is now 29,4512. This aggregate number is still low on a per-capita basis given India's substantial population. While there may be concerns that the case number is underestimated due to the low per-capita testing level in India (around 492 tests per million people), the percentage of positive results (infections/tests) remains low at 4.4%, despite the testing of mostly higher-risk cases3.

The lockdown seems to be working as the five-day compounded daily growth rate in infections has slowed to 7% (27 April) from 18% (31 March). Also, the infections are quite concentrated: On 21 April, there were 61 districts (out of total 717 districts in India) that had greater than 50 cases4.

We acknowledge the vast uncertainties associated with a pandemic; however, there are some positive signs emerging in India: (a) a lower incidence of positive test results, (b) a falling rate of growth in new infections, and (c) quick identification of hotspots and robust measures taken to stop the spread of the virus.

In the near term, we still forecast the number of new infections to rise albeit at a decelerating pace. That said, over the next month, we expect to see a gradual "exit plan" from the lockdown. Indeed, some businesses have already been allowed to resume operations with social distancing for some of the lesser affected districts.

In response to the economic impact of the lockdown, March saw the government announce a stimulus programme (worth approximately US$23 billion or around 0.8% of GDP) that provides food and income security to low-income households. The package was distributed via cash transfers, employment support, credit support, and food support.

While these are critical initial moves to support the economy, we believe that bolder steps from policymakers are needed to address this unprecedented economic threat. The size of the current stimulus package is inadequate to effectively counter the estimated loss of output (approximately 6–8% of GDP).

We think that more measures will be announced in the coming weeks, as the exit strategy from the lockdown is formulated. This will be vitally important: without adequate countermeasures, a substantial loss of output may create a second-order impact in consumption patterns and amplify the cyclical pressures that were visible in the economy even before the lockdown.

While there is a valuable debate about whether India has the fiscal room to afford a substantial stimulus, it is important to note that the size of India's support programme is by far the lowest (as a percentage of GDP) among the top-ten global economies5. We believe that policymakers can find a way in such unprecedented times, and it can be found through adopting unconventional policies.

If policymakers make it abundantly clear that unconventional policies will be time and event specific and would be unwound once its objectives are achieved, we think financial macro stability will not be impacted. On the brighter side: investors could also start focusing on whether economic growth can return in the medium term should a targeted fiscal package be able to contain the immediate downside.

The Reserve Bank of India (RBI) has also stepped in to provide adequate liquidity to counter a sudden economic stop, which would negatively impact firms' revenues and cash flows: Recent actions include:

We think these measures will stabilise market functioning and ease financial conditions. Once the government decides on the final fiscal package, we would expect more steps from the RBI, including how to manage the bond supply.

While the administrative lockdown is necessary to avert a public health crisis, it will come at a notable economic cost as it has disrupted activity in most sectors. Our base case remains that under the current lockdown assumptions7, we expect an output loss of 6–8% of annual GDP and a higher fiscal deficit as tax collection should be lower.

We expect a gradual economic recovery as a certain amount of social distancing will continue over the medium term to avoid another wave of infections. In turn, this will cause an uneven recovery across different sectors. Businesses that depend on the gathering of people, such as retail, hospitality, tourism, cinemas, exhibitions, and construction sites, may see ongoing restrictions and weaker activity. On the other hand, sectors that cater to social distancing, including personal mobility, packaged foods, telecom, and home improvement, automation, white goods, and consumer electronics, are likely to recover faster.

Despite the favourable long-term backdrop for Indian equities, the economy faced specific cyclical challenges even before the COVID-19 pandemic:

The ongoing lockdown in India will amplify these existing cyclical challenges. Unless the economy is bolstered with adequate stimulus measures from the government, the sudden economic stop will affect income and savings.

Before COVID-19, the government and the RBI had already started to counter the cyclical challenges. The government focused on longer-term structural policies to encourage investment and job creation, while the RBI supported with monetary policies to cut rates and push out liquidity to the real economy.

Despite these two short-term challenges, we retain our long-term view on India. Indeed, we have detailed in our past notes that our constructive Indian equity outlook is founded on the structural reforms that were undertaken by the current administration in its first term. These moves laid the foundation for a formalisation-led growth through the drivers that we named the '4 Fs'.

We had also argued that with these fundamental building blocks in place, the re-elected Indian government has a unique opportunity to revitalise economic growth through the '3 Rs':

We believe the 3Rs should help address the cyclical growth challenges through higher government spending, increased savings for the private sector and households, and more job opportunities by encouraging new investment.

At the same time, some elements of the 3Rs may face delayed implementation due to COVID-19, such as Recycling (the privatisation of SOEs). Policy makers will need to adopt innovative solutions to bridge the gap. We believe they will find solutions through increased government spending and other policy measures.

We believe Indian policymakers are in a relatively good position to accomplish this due to the country's ample foreign exchange reserves and low level of short-term foreign debt (which lends to a robust capital account). In addition, the inflation outlook remains benign, and whilst the fiscal situation could deteriorate, the recent sharp fall in crude prices could swing the current account deficit to a surplus.

Indeed, the sharp correction in crude oil prices should remain a key positive catalyst for markets, as India is a large importer of crude oil. India will benefit from a lower import bill and better current-account balance. Our estimates suggest that each US$10 drop in crude oil prices helps India's current account balance by roughly US$13 billion10. This translates into higher domestic savings and provides room for the RBI to remain accommodative, as a US$40 fall per barrel could result in approximately US$50 billion of total savings.

Overall, the COVID-19 pandemic will accelerate the formalisation-led growth story that underpins our long-term bullishness on Indian equities. The listed market, which is represented by the organised sector, should emerge more robustly and gain market share. It will require both financial strength to overcome this difficult period and management bandwidth to pivot strategy and operations as economic activity resumes under the shadow of social distancing.

In the current environment, we believe the following type of companies and sectors are likely to succeed:

(1) Companies that benefit from new social distancing and work from home norms after economic activity resumes post-lockdown. Sectors includes personal mobility plays (two wheelers), home automation and improvement plays (consumer electronics, white goods, decorative paints), personal hygiene products, packaged foods, and telecom.

(2) Import substitution plays benefitting from government policy of encouraging domestic manufacturing (EMS companies), as well as a diversification of production away from China due to the trade war (specialty chemicals and pharma). We also expect select IT services exports to benefit as its enabling remote working across the globe.

Finally, we also believe that some companies are less likely to succeed: sectors likely to suffer from social distancing are retail, leisure and travel, hospitality, and commercial real estate. Also, companies with high fixed costs and debt on their balance sheet should face a disproportionate downgrade risk during the lockdown.

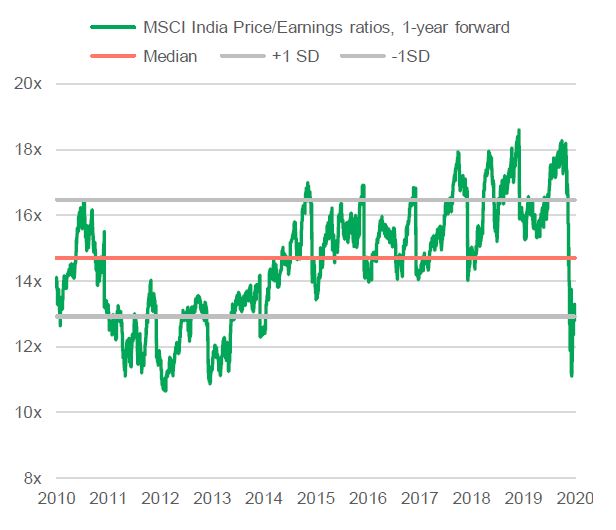

The Indian market corrected in line with its global counterparts in March and April, and its valuation is now below the 10-year median level (see Chart 1). Whilst more earnings downgrades are possible in near term, we believe it will normalise in medium term led by the beneficiary sectors. We believe that India remains a growth story that is local, defensive, bottom-up and good opportunity to gain market share in exports.

Lastly, investors should also be aware of risks to our medium-term constructive view. For COVID-19, these include: a rebound in the infection curve or a second wave of infections as the economy opens back up. Risks also exist if the current lockdown period would be extended, or if the government would provide a lower than expected level of fiscal support.

1. Measures included: border closures through the suspension of visas and domestic measures, such as the closure of schools, colleges, and public places.

2. MOHFW India, as of 27 April 2020 (www.covid19india.org).

3. Data as of 22 April 2020, MOHFW India (www.ourworldindata.org,)

4. Credit Suisse Research, as of 21 April 2020.

5. IMF, available at https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19

6. The facility allows banks to borrow at the policy rate and buy commercial paper, investment grade bonds etc. and cut the cash reserve ratio by 100 bps (giving more liquidity to banks).

7. The strictest form of the lockdown will be in place for roughly 1 month.

8. RBI Announces Two Long-Term Repo Operations in March. Bloomberg, 25 February 2020.

9. RBI, Citigroup, February 2020.

10. Manulife Investment Management, 12 March 2020.

11. Bloomberg, as of 24 April 2020.

Asset allocation views on SpaceX IPO, Reopening of Strait of Hormuz, and the BOJ rate hike

The Multi Asset Solutions Team (MAST) provides asset allocation views on three recent developments that could influence markets in different ways: the SpaceX Initial Public Offerings (IPO), the reopening of the Strait of Hormuz, and the Bank of Japan’s (BOJ) rate hike. In our view, these events create mixed signals across growth, inflation and liquidity. Overall, the backdrop still appears uneven, and this may support a measured and selective approach to asset allocation rather than a broad increase in risk.

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()