06 May, 2021

Frances Donald,

Global Chief Economist and Global Head of Macroeconomic Strategy, Multi-Asset Solutions Team

Nathan W. Thooft, CFA,

Co-Chief Investment Officer, Multi-Asset Solutions Team and Global Head, Senior Portfolio Manager, Asset Allocation Team

Luke Browne,

Senior Portfolio Manager and Head of Asset Allocation, Asia, Multi-Asset Solutions Team

Sue Trinh,

Senior Macro Strategist

Paul Kalogirou,

Client Portfolio Manager

To call 2020 "unprecedented" wouldn't begin to do justice to the depth of challenges individuals and organizations around the world found themselves unexpectedly confronting over the past year—nor the speed with which those challenges arrived.

It was early January 2020 when news broke of a pneumonia-like virus circulating in Wuhan, China; before the end of the month, the World Health Organization had declared COVID-19 a global public health emergency and less than six weeks later, many developed nations around the world had implemented broad-based lockdowns in an unproven attempt to contain a virus the medical community knew alarmingly little about. Businesses and schools were quickly shuttered. Those who could work from home did; those who couldn't found themselves facing a precarious and uncertain financial future almost literally overnight.

While the cost in lives and livelihoods the virus has extracted over the past year is enormous, there is good news at hand and more on the horizon: The lethality of the virus is decidedly not as bad as some had originally feared, doctors and medical professionals have become much better at treating it, and multiple vaccines are already being administered. And while a surge in variants and a third wave of the virus are still weighing heavily on many parts of the world, there are many reasons to be optimistic that 2021 will improve upon 2020.

But despite the near-universal desire to turn the page on 2020 and return to some version of the "old normal," the pandemic and the changes it has brought with it will almost certainly transform societies in some lasting ways, both big and small. This paper takes a closer look at those changes, the economic and market implications they suggest, and how investors might position their portfolios to benefit from them. We break down both the short-term tactical opportunities we see unfolding as well as some of the longer-term, more permanent shifts likely to transform the economy and the way investors think about the markets.

Naturally, not all jobs can be done from home, but one of the more immediate effects of the pandemic was to launch a massive social experiment to discover exactly how many could.

Before COVID-19, estimates suggested that no more than a quarter of all full-time employees worked from home, but since March that number has climbed to at least 37%; some estimates suggest the actual figure is closer to 50%. In certain industries and locales, the current number is significantly higher than that: Computing, legal, business, education, and finance occupations all reported at least 88% of their employees working from home.1

While unexpectedly changing the daily work habits of large swaths of the population may seem like a mostly personal disruption, it has had significant knock-off effects on the economy in some profound ways.

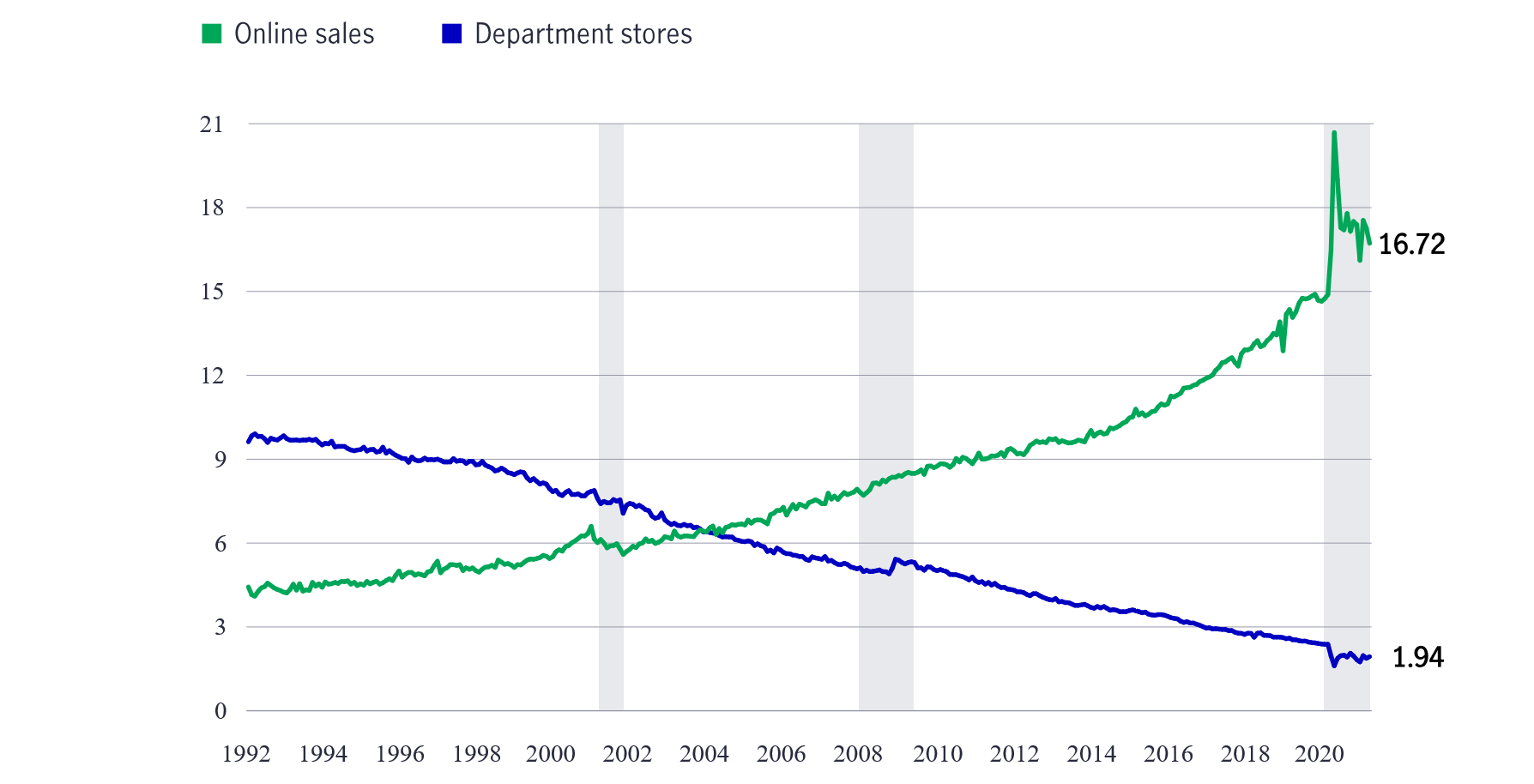

The dramatic shift in the demands placed on the home—from serving primarily as family sanctuaries to becoming much more multifunctional and versatile spaces—has brought with it a number of changes in patterns of consumption. E-commerce and streaming services, for example, have experienced huge increases in demand as more and more consumption has occurred within the home; that single shift in where buying decisions are made has produced some clear beneficiaries. Brick-and-mortar local businesses, already under decades-old pressure from the shift to online buying habits, will likely continue to lose market share to their digital multinational competitors.

Share of total retail sales (%)

Source: U.S. Census Bureau, Macrobond, Manulife Investment Management, as of April 15, 2021. Grey areas represent recessions.

The demand for data itself will likely see a sharp increase. Companies that have successfully weathered the relocation of entire workforces—from out of the office building and into the home office—will find their need for physical space shifting to a need for more digital space. Supporting remote workers through file storage, videoconferencing, and collaborative platforms requires significant investment in cloud-based infrastructure.

Beyond the field of business, the healthcare and education fields also both experienced dramatic rises in demand for data as telemedicine and remote learning both leapt into the limelight this year (with decidedly mixed initial results). Governments, too, may discover an increased appetite for data at multiple levels. Contact tracing, early-warning systems designed to spot flare-ups, and healthcare databases all require significant digital footprints. A great deal of disparity exists between those governments that were early adopters on this front (e.g., South Korea) and those that may feel compelled to catch up (the United States, Canada, and much of Europe).

The bottom line is that those segments of the economy levered to rising demand in digital consumption channels look well positioned for the years to come; those that cannot adapt (i.e., shopping malls) will likely be left behind.

The pandemic clearly highlighted the vulnerabilities in global manufacturers' supply chains this year, and there are a number of changes already emerging in response. Automation, we believe, is an area that will likely see accelerating demand in a postpandemic world. The competitive advantage in being able to perform vital production line functions with minimal staff is, by this point, self-evident, and we believe that trend is only beginning to gather momentum. Artificial intelligence and robots will permeate general-purpose machinery in areas such as food, healthcare, consumer goods, and e-commerce, we believe, helping to better insulate supply chains from exogenous shocks.

The risks exposed by the pandemic aren't the only factors driving this trend. Aging workforces in many parts of the world combined with falling prices as automation technology becomes both more accessible and more efficient should speed the rate of adoption. Both providers of automation technology and those sectors that implement it most effectively stand to benefit, we believe.

In our view, expectations of a profound decline in business and personal travel in a post-COVID world are likely unwarranted. But we do see evidence that travel will be more regional than the trends of previous years indicate. Long multinational business junkets are likely to be curtailed, while international vacations and cross-country trips are likely to transition to outings closer to home.

Migrant workforces may also play a smaller role in the overall global economy in a postpandemic world. The desire and ability of individuals, skilled or not, to cross international borders for work is likely to take several years to return to 2019 levels; some regions and industries where automation and remote work arrangements accelerate may not return to those levels at all.

It's hard to overstate the significance of China in global trade. One study estimates that roughly 12% of all imports globally originate in China, with levels closer to 20% in the European Union, United States, and Japan.2 For companies that rely on overseas supply chains, that kind of concentration of risk in a single geography represents a risk that today looks increasingly imprudent. For that reason, we envision a deliberate deemphasis and diversification away from China for developed-market supply chains—and we see a corresponding move by China to deemphasize its reliance on Western markets, accelerating the expansion of its internal value chains and nurturing the growth of a consumer-driven economy.

There have been numerous comparisons between the global financial crisis and the lockdown-driven economic collapse of 2020; one comparison worth a closer look is the government fiscal and monetary response.

In 2008, when the global financial crisis loomed, central banks unleashed unprecedented levels of stimulus, including the United States' first foray into quantitative easing. Government spending programs generally played a smaller role to monetary policy, with some regions toeing a budget austerity hardline.

At the beginning of the COVID-19 recession, central banks around the world once again intervened, this time expanding their toolbox even further than in 2008 to include, importantly, direct support of credit markets. However, as winter set in on the northern hemisphere in Q4 2020 and cases spiked again, the recovery's momentum stalled. Subsequent social distancing measures have kept a lid on businesses' operating capacity and job losses began to affect aggregate demand. Problematically, while central banks have been able to provide support to the economy and to financial markets, the crux of the economic headwinds has remained the virus and the pace of vaccinations. As such, monetary policy appears to have reached its limits in the fight against a global pandemic.

Fortunately, governments, particularly in the United States, seem poised to fill the gap and enter a phase of higher baseline structural levels of support. The rollout of vaccines around the world will eventually diminish the urgency of new spending initiatives, but today there remains an opportunity for direct investment in government-favored projects, including infrastructure, education, and greater incentives for investment in low-carbon technologies. We see the emphasis on fiscal spending as the appropriate ongoing tool for economic support to persist, contributing to a larger role for government and, importantly, more sovereign bond issuance.

The pandemic has reminded us how important it is to select companies that can adapt to new ways of consumption and maintain existing levels of service—or even add value—in the absence of fewer physical touchpoints. We've also seen a shift away from profit maximization toward corporate social responsibility that considers the interests of all stakeholders, including clients, employees, shareholders, the community, and the environment.

As a result, we're seeing investors increasingly turn to sustainable investments that track environmental, social, and governance (ESG) factors. According to Morningstar, active funds that invest according to ESG principles have attracted net inflows of more than $70 billion globally in the second quarter of 2020, pushing assets under management in the products to a new high of just over $1 trillion.3

This significant global inflow into ESG products may foretell shifting priorities for other forms of capital allocation. Poverty and disease have long traveled hand in hand, and as income disparities continue to be exacerbated by the pandemic, so too will health outcomes, both between and within nations. Even among OECD member countries, we've seen a plateauing of the ultimate health metric—life expectancy—in the 21st century.4

But there is reason for optimism. There is today clear evidence of greater consumer engagement in health, and significant advances being made literally every day in the creation of better treatments and therapies and the adoption of new and significant health technologies. After all, in a world concerned about pandemics, health considerations will remain top of mind as governments and corporations formulate their post-COVID-19 planning to address the well-being of citizens, employees, and stakeholders.

Economies around the world have slowly started to reopen, albeit unevenly and subject to their vaccination rollouts. In terms of macro data, we've seen encouraging improvement in unemployment figures, with the pace of job creation now sharply accelerating in the United States. Manufacturing data in the United States has surged to its highest level in decades, suggesting positive prospects for the manufacturing side of the global economy, particularly relative to the consumer. More recently, the latest U.S. Purchasing Managers' Index data in 2021 is showing not only a stronger recovery in manufacturing, but also a sizeable improvement in services activity.

Looking at the opportunity set in 2021, we see the merit in taking a balanced approach, tilting toward sectors that are poised to benefit from a continued economic recovery, while also incorporating some more cyclical areas that look undervalued.

We still see upside potential in 2020's market leaders, including tech, communications, consumer discretionary, and growth stocks in general, but we're balancing those areas with targeted positions on the value side, such as industrials, materials, metals and mining, and selectively with financials.

While we believe there are a number of meaningful short- and long-term opportunities emerging as the world finds a new kind of post-COVID-19 equilibrium, not all of them are easily accessible for investors—not even global institutional asset managers. Some may be too nascent to reliably take advantage of, while others may not offer the necessary scale to add meaningful value to a portfolio.

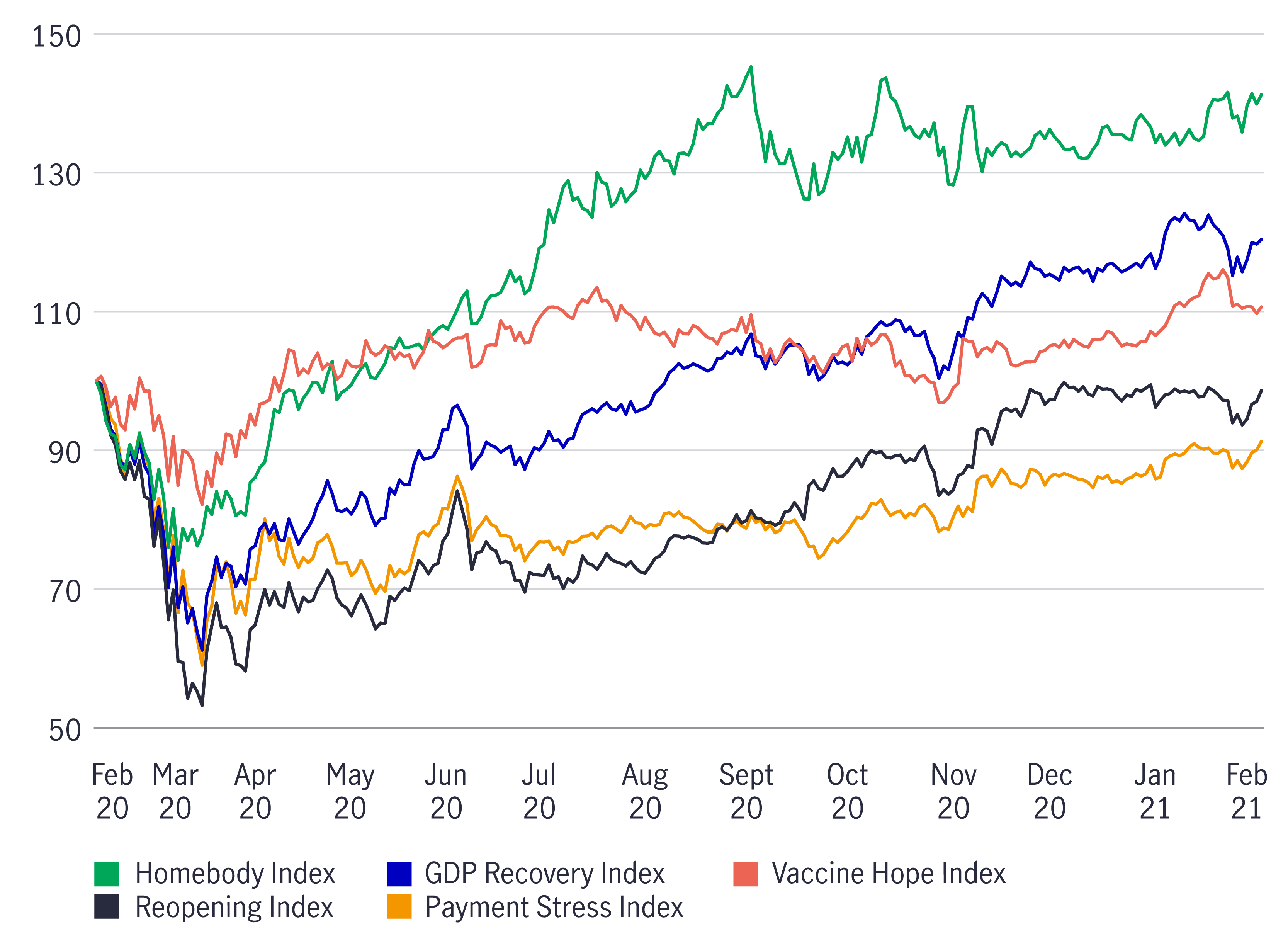

Nonetheless, these underlying trends can still be monitored and can certainly shape the way we think about the macro environment—a shift away from traditional premises toward emerging, unconventional macro trends. Since the outbreak of the COVID-19 pandemic, we've been tracking a number of alternative data sets, such as the Vaccine Hope Index, Reopening Index, Homebody Index, GDP Recovery Index, and Payment Stress Index. While indexes like these represent just one way we're able to glean insight about the way these investment themes are manifesting themselves in the markets, we believe adding this kind of hard data to our thematic observations is crucial to formulating actionable investment ideas.

S&P subindex performance, indexed to 100, as of Feb. 20, 2020

Source: Macrobond, Standard & Poor's, Manulife Investment Management, as of February 25, 2021.The indexes above consist of various subsectors of the S&P 500 Index as compiled by Macrobond. It is not possible to invest directly in an index. For more details on the subsectors in each index, see the disclosures below.

When thinking about fixed income from a multi-asset perspective, in a world where investors are feeling increasingly compelled to reach for yield, the most attractive opportunities lie outside of the sovereign debt space. But that also suggests to us that the overall valuation for equities should be thought of in a new light.

It's conceivable that equities trade at slightly higher multiples over the foreseeable future in large part because the comparison to fixed income isn't the same as it was over the past 30 years; while bond yields have ticked up modestly, they are still exceptionally low by historical standards In such an environment, investors may continue to reward companies that have growing earnings stream, regardless of sector, and those companies may very well trade at higher multiples than they have in the past. We believe that possibility makes it somewhat more challenging—and important—to identify which sectors and securities truly present the opportunity for growth at a reasonable price.

1 "How Many Jobs Can be Done at Home?"" Jonathan I. Dingel and Brent Neiman, Becker Friedman Institute, June 2020.

2 "The Post-Covid Economy," OECD, Barclays Research, August 2020.

3 "ESG funds attract record inflows during crisis," Financial Times, August 10, 2020.

4 "Health Equity in England: The Marmot Review 10 Years On," The Health Foundation, February 2020.

5 Manulife Investment Management's multi-asset solutions team, as of March 16, 2021.

2026 Mid-Year Outlook Series: Global Macroeconomic

The Middle East conflict remains a key macro theme in H2 2026, with geopolitical uncertainty persisting despite a tentative US-Iran deal. Even if Strait of Hormuz blockades are lifted, we have low conviction that commodities traffic through the region will resume swiftly, with some degree of geopolitical uncertainty likely to persist through the rest of this year.

Latest asset allocation views for Asia Q2 2026

Three key global themes for latest asset allocation view in Q2 2026 are: 1.Middle East conflict: energy risk and macro uncertainty; 2. AI: bubble or build-out; 3. Diversification isn’t dead; it’s different.

EQDP in Context: Key Implications for the Market

Read more![]()