11 January 2023

Kenglin Tan, Senior Portfolio Manager, Equities

As we sail into a new year, we believe that some of the macro headwinds and regional dynamics might continue to linger and impact Asian equities in 2023 – namely high interest rates and a prolonged war between Russia and Ukraine. However, the effects of the pandemic will wane, and economic growth is expected to expand – albeit at a rate that is well below the average rate seen over the preceding two decades.

Going into 2023, we remain vigilant on the impact of tighter financial condition on Asia. Barring any financial shocks, we see Asia’s economic growth profile as stronger relative to developed markets. Growth in the region is expected to be supported by the normalisation of economic activities in China and further recovery from the pandemic in other parts of Asia. The attractiveness of the region is accentuated by stocks trading on undemanding valuations.

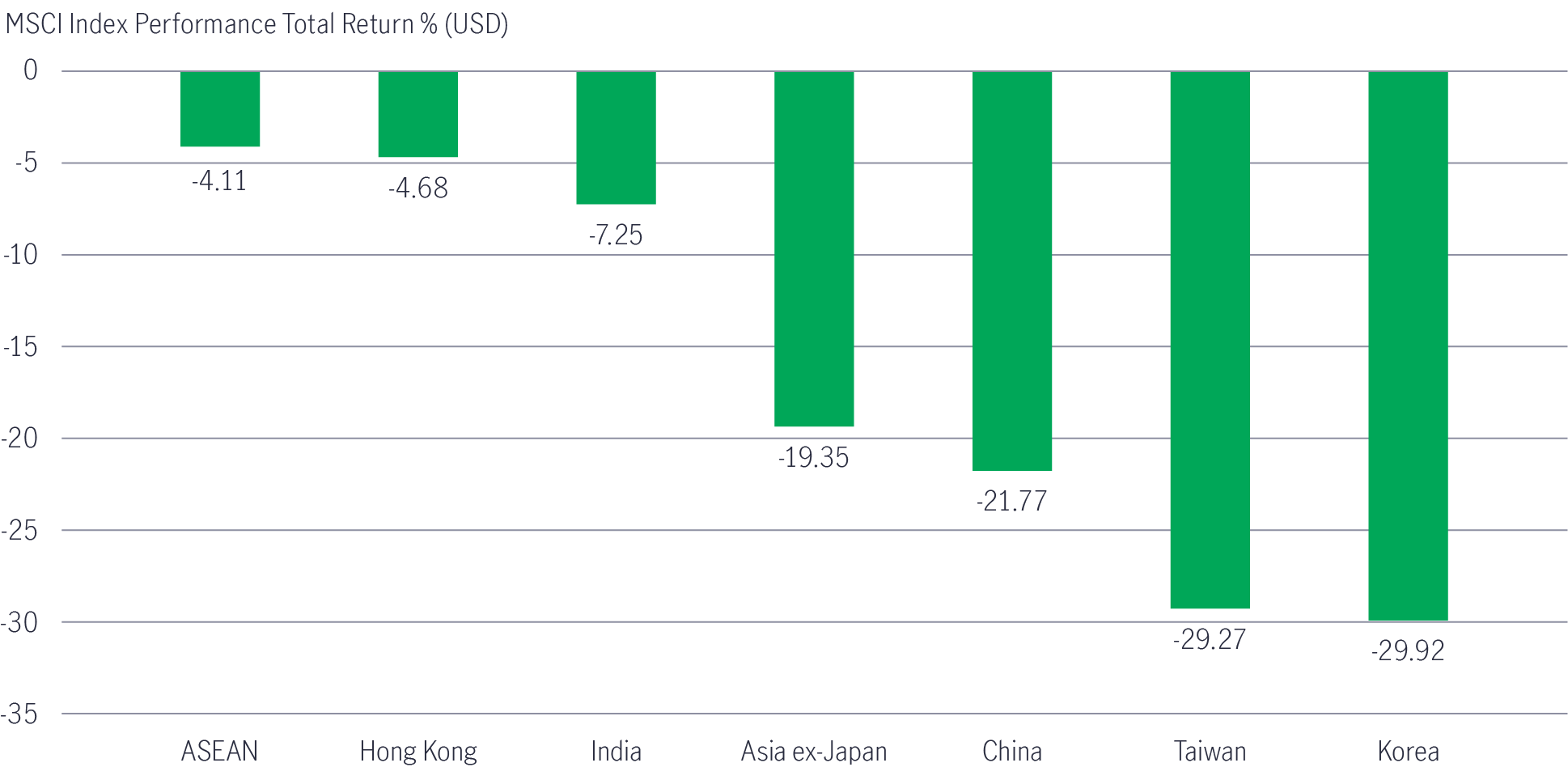

In retrospect, three quarters of the year were filled with consecutive jumbo rate hikes and elevated inflation. Overall, MSCI Asia ex-Japan equities posted 19.35% loss in 2022 in US dollar terms which were largely driven by the North Asia markets. China and Hong Kong equity markets rebounded in the last quarter on the back of loosening of strict COVID measures. The near 30% drawdown in Taiwanese and Korean equities were a result of weaker demand in tech and led to elevated inventory levels and de-stocking of chips and electronics. ASEAN was the relative outperformer given the attractive valuation, resilient fundamentals at the corporate and country levels led by Indonesia and Thailand. Indian equities were also resilient relative to the overall Asia region as earnings growth and strong retail fund flows were supportive of market performance.

Chart 1: 2022 market summary

Source: Bloomberg, 31 Dec 2022; ASEAN equities are represented by MSCI AC ASEAN USD Index, Hong Kong equities are represented by MSCI Hong Kong Index; Indian equities are represented by MSCI India Index; Asia-ex-Japan equities are represented by MSCI AC Asia ex Japan Gross Total Return USD Index; China equities are represented by MSCI China Index; Taiwan equities are represented by MSCI Taiwan Index; Korean equities are represented by MSCI Korea Index. All are total return in USD.

Towards the end of fourth quarter, investors got excited and felt relieved by a slower pace of rate hikes in the US Federal Reserve (Fed). However, we believe the impact of higher interest rate has yet to be felt through the system. We prefer to err on the side of caution.

We believe that the aftermath of the various global macro headwinds will linger into 2023: core inflation is expected to remain elevated underpinned by a strong labour market and higher costs related to the recalibration of global supply chains; interest rates may stay higher for longer; and more importantly, the full impact of 2022’s policy tightening has yet to work through the system. Bouts of liquidity tightness may pose risks to the stability of the financial system, with opportunities being stock specific rather than the broader market.

Although China was restricted by various headline issues ahead of the 20th National Congress in mid-October, the government is now taking measures to ease some of the economic pressure: The recent relaxation of its zero-covid policy and measures to ease funding pressure on the property sector have prevented further deterioration in the country’s economic conditions. The government is expected to announce more policies to support and stabilise economic growth going into 2023.

On a mid-to-long term basis, we believe the Chinese government will focus on national security, self-sufficiency, food security, social stability, and common prosperity. Amidst a paradigm shift in China’s development model, we have assumed a lower long-term growth trajectory and a higher risk premium for Chinese assets. Against this backdrop, we have identified opportunities in the following segments which we feel are consistent with the leadership’s objectives:

Taiwan is grappling with the high inventory built up in the semiconductor sector over the past 12 to 16 months – due to the expected slowdown in international demand and de-stocking of electronics. Indeed, the utilisation rate of some chip foundries has fallen by as much as 80%, and it could take around six to nine months for the industry to clear this excess stock. In addition, heightened China-US tensions and recent policy outcomes are likely to result in an erosion of earnings for companies supplying to China. Many companies are going to have to recalibrate their geographical capacity expansion, which is likely to inflate costs, whilst potentially alienating demand. We, therefore, expect underperformance in the technology hardware supply chain in the coming quarters. From an investment perspective, this negative sentiment is offset by relatively undemanding share-price valuations that present opportunities over the longer term.

Simultaneously, demand for auto technology is one of the very few bright spots left in the sector, and we are capturing growth in this segment through the supply chain of electric vehicles. We are keeping a watchful eye on new tech products that could drive demand in fields such as augmented reality (AR) or virtual reality (VR). Another area of interest is the adoption and upgrade of EVs. The EV sector is triggering strong demand for semiconductor chips, but we are somewhat cautious as consumer desire for EVs could be tempered by the rising interest-rate environment with borrowing costs.

Similar to Taiwan, Korea’s tech sector is digesting excess chip inventory. But it is also being challenged by slower demand for smartphone memory chips amid sluggish consumer demand.

On the other hand, Korea’s financial sector looks more appealing, given the country hopes to be re-classified as a developed market in global bond indices. The government is trying to introduce more investor-friendly policies, especially within the banking space. Valuations appear attractive with some institutions trading at forward price-to-book ratios which we believe are cheap relative to their return on equity. High single digit dividend yields also help augment the risk-reward profile for select Korean banks2.

Elsewhere, we also like some of Korea’s domestic consumer plays, especially within e-commerce, where new companies are gaining market share from incumbents.

ASEAN markets have held up relatively well in 2022 versus other Asian markets due to their economic resilience and vastly improved foreign debt composition relative to history. In addition, many ASEAN nations stand to be beneficiaries in the global diversification of supply chains away from China, the so-called “China plus one” strategy. Economic growth of the region is expected to outperform other developed markets and emerging markets in LATAM and EM Europe.

Unlike previous cycles, key macro-economic indicators in the region have improved and ASEAN economies are in much stronger positions compared to the previous cycles. The region’s current accounts are in better shape and trade is flowing smoothly.

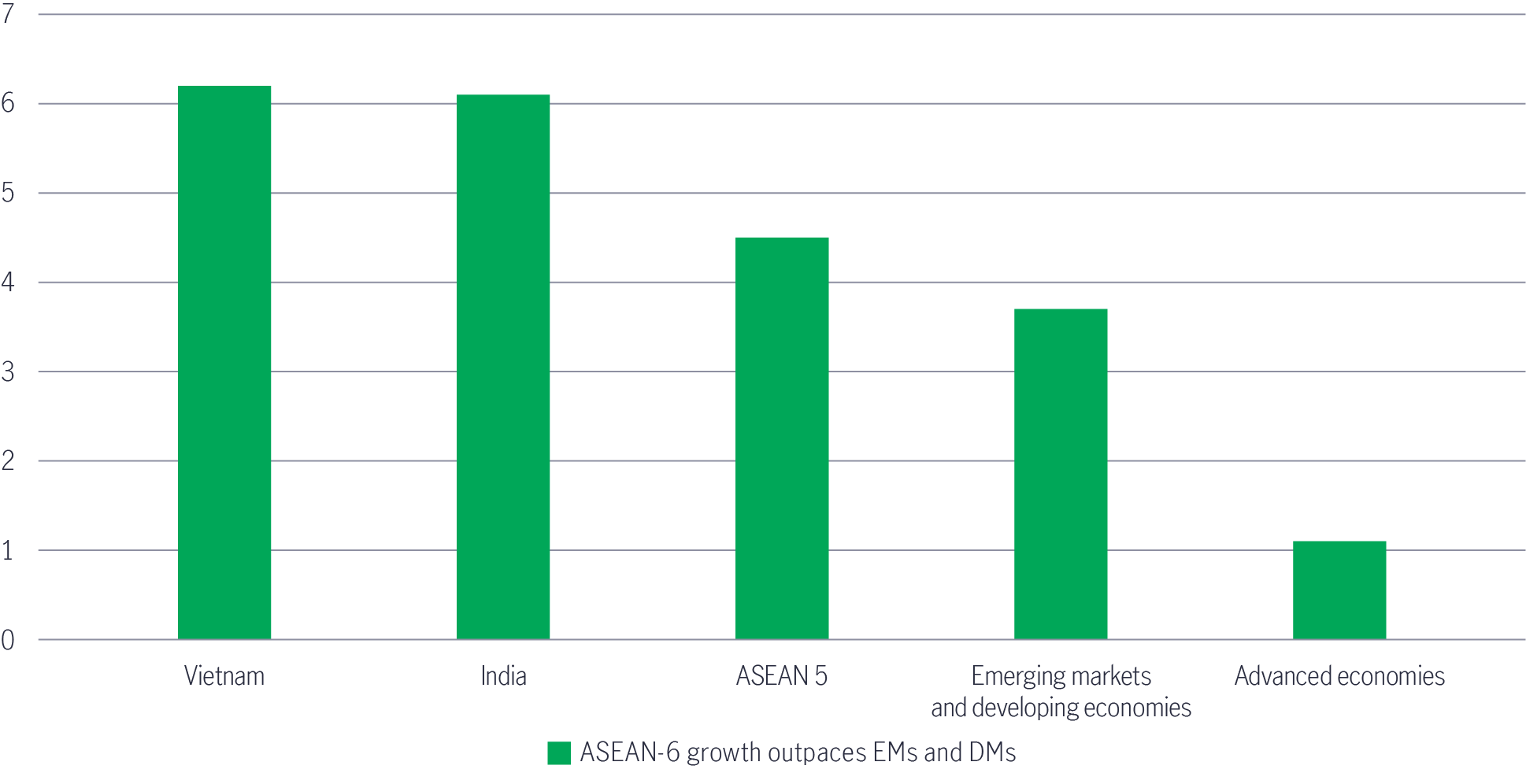

In growth terms, China used to outpace ASEAN, but China’s GDP growth estimate of 5% is expected to converge with the core ASEAN-5 economies of Indonesia, Malaysia, the Philippines, Singapore, and Thailand, which are also averaging around the 5% level, while India is heading towards 6%.

Chart 2: ASEAN-6 growth outpaces emerging markets (EMs) and advanced economies

Source: International Monetary Fund, World Economic Outlook October 2022; Regional Economic Outlook for Asia and Pacific October 2022.

We continue to view ASEAN as one of the growth spots in Asia in terms of corporate earnings growth, supported by undemanding valuations. Besides, there are deeper reasons for the investment case of this economic bloc:

The Regional Comprehensive Economic Partnership (RCEP) group is an important driver and growing source of global foreign direct investment (FDI) for ASEAN. From 2015-2022, about 40% of investment in ASEAN come from RCEP members, of which 24 % comes from non-ASEAN RCEP member countries. For example, Malaysia and Vietnam continues to receive FDIs in the electric and electronic segment. Singapore has become the preferred option for wealth management and financial services within Asia, benefiting from wealth-management fund flows from China and even Hong Kong.

As global brands and manufacturers diversify their supply chain, they adopted the strategy of investing in other Asian countries in addition to China. ASEAN is a beneficiary for this trend with opportunities abound in different areas. From a tech perspective, the manufacturing of electronic goods and other industrial products is shifting to Malaysia and Vietnam. Indonesia and Thailand are forming an EV supply chain in ASEAN, catering both to domestic and external demand. In particular, Indonesia’s abundant supply of nickel with a large domestic auto market puts the country in a strong position to complement growth in the EV supply chain in “ex-China Asia”.

A key area of growth in Southeast Asia will be medical tourism. The cost of care in the region is notably lower than in most developed markets. Among the popular ASEAN destinations for medical travel, Thailand, Singapore, and Malaysia had become major players, driving inbound travel to the region for their competitive rates, top-line medical care, technological advancement, and renowned medical expertise with world-class clinical services to overseas visitors, often from the Middle East and frontier territories Indeed, Thailand is benefiting from a recovery in tourism post-pandemic whilst also benefiting from healthcare tourism. According to the Tourism Authority of Thailand, Thailand will exceed its most-recent target for foreign tourist arrivals by about 15%. China’s reopening is set to further boost tourist spending in the country.

Meanwhile, even though it lags behind China, the digitalisation of ASEAN economies remains on an upward trajectory. The region is projected to be one of the world’s fastest-growing data centre markets in the next few years, exceeding the growth in North America and the rest of Asia-Pacific. According to ASEAN Secretariat, the investment needs for 5G infrastructure in ASEAN are significant, estimated at about $14 billion in annual capital expenditure between 2020 and 2025 to upgrade telecommunication facilities, networks, and equipment to 5G requirements. It’s also expected that Southeast Asia’s digital economy will register strong CAGR growth from 2022 to 2025 in travel, food and transport as economy continues to reopen and recover.

India’s long-term structural growth story remains attractive. For now, though, earnings growth is moderating, and stocks are highly valued. That aside, we are also mindful of how the country balances its infrastructure gap with the volume of inward investment. Moving into 2023, India has already tackled inflation with aggressive interest rates, and with the price of oil declining, rising costs may be less of an issue in the months ahead. In addition, we believe that India’s twin current and budget account deficits should be contained, which could eliminate some risk from the financial system.

Looking forward, we believe that investors could take the view that the world is shifting towards a tighter financial condition and higher cost of capital. We expect stronger players trading on attractive valuation to benefit from a market recovery. A good number of small and mid-sized firms with strong balance sheets and cash flow are trading on cheap valuations. We have opted to avoid overvalued unicorns with poor cash flow generation and weak balance sheets and would rather focus on regional companies that are recovering from pandemic-related disruption and have been overlooked. Overall, we remain cognisant of market allocation, but will also position our portfolios to capture the most attractively valued and growth opportunities across the region.

1 Bloomberg, as of 31 December 2022.

2 Source: Bloomberg, MSCI Korea Bank index 31 December 2022.

3 ASEAN 6 represents ASEAN 5 (Indonesia, Malaysia, Philippines, Singapore and Thailand) and Vietnam.

4 The Regional Comprehensive Economic Partnership (RCEP) is a free trade agreement (FTA) between the ten member states of the Association of Southeast Asian Nations (ASEAN) (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, Vietnam) and its five FTA partners (Australia, China, Japan, New Zealand and Republic of Korea).

Global Macro Outlook Q3 2023: The long and winding road

At the time of writing, only the eurozone and New Zealand have slipped into recession (as defined by two consecutive quarters of negative growth). But don’t pop the champagne just yet: We see this as a case of recession postponed rather than canceled. Read more.

Asian High Yield: Building resiliency amid volatility

Although emerging from a difficult period, Asian-high-yield is positioned to weather the current market volatility due to regional economic strength and unique asset class characteristics.

Global Healthcare: Enhanced innovation in a post-COVID environment

We discuss the attractiveness of allocating to the healthcare sector in the current economic environment and outlines why it warrants a long-term allocation.

2026 Mid-year outlook: Global Semiconductor

The semiconductor sector remains a key enabler of the global economy, underpinning artificial intelligence (AI), cloud computing, and electrification. As highlighted in our earlier insights, it represents a broad ecosystem supported by structural demand and real infrastructure investment. Following strong year-to-date performance, we see growing conviction that momentum can extend into the second half of 2026 and into 2027, driven by earnings strength, sustained capital investment, and early-stage AI adoption.

2026 Mid-Year Outlook Series: GEDI

Against a highly uncertain backdrop in the first half of 2026, Manulife’s Global Equity Diversified Income (GEDI) Fund (‘the Fund’) posted resilient performance with relatively lower volatility. This result was driven by the Fund’s four investment pillars, which favour an income-centric approach, coupled with global diversification across growth, value, and income equities. In this 2026 Mid-Year Outlook, Paul Kalogirou, Head of Client Portfolio Management, Asia & Global Multi-Asset Solutions, explains how the Fund’s unique structure allows for consistent income generation and potential upside across the market cycle, while also identifying key opportunities and risks for the second half of the year.

2026 Mid-year Outlook Series: Diversified Real Assets

Global supply chains are resetting under deglobalisation and geopolitics, shifting from global efficiency to more expensive regional resilience, embedding higher structural costs. At the same time, artificial intelligence (AI) is emerging as a new demand driver, accelerating investment in power, infrastructure, and materials. Against this backdrop of structurally higher inflation and dual demand pressures – from both supply-chain rewiring and AI capital expenditure – we believe real assets may play an increasingly important role in portfolios, offering exposure to long-term secular growth and AI trends.

![]()